Transmission Systems Market Size, Share

Report Overview

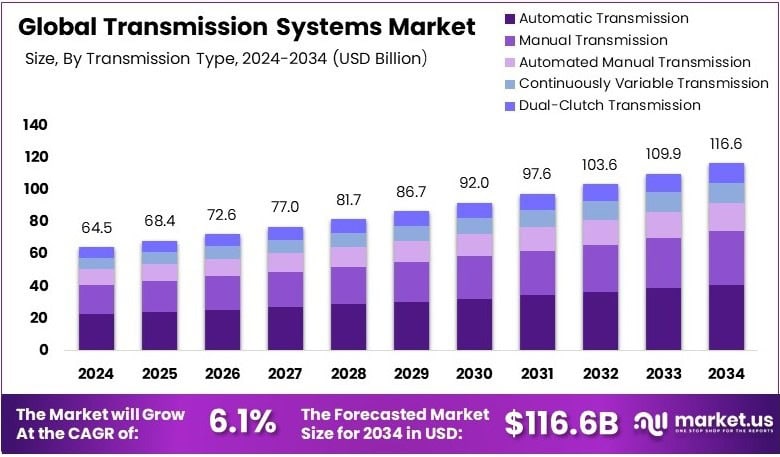

The Global Transmission Systems Market size is expected to be worth around USD 116.6 Billion by 2034, from USD 64.5 Billion in 2024, growing at a CAGR of 6.1% during the forecast period from 2025 to 2034.

Transmission systems are parts of a vehicle that transfer engine power to the wheels. They control the speed and torque of the vehicle. Transmissions help improve fuel efficiency and driving comfort. There are different types, including manual, automatic, and dual-clutch systems, depending on vehicle type and performance needs.

The transmission systems market involves the production, sales, and innovation of transmission units used in vehicles. It covers various technologies across personal, commercial, and electric vehicles. Market growth is driven by rising vehicle sales, demand for automatic systems, and advancements in gear shift technology and fuel efficiency.

Transmission systems are a key part of how vehicles operate. They manage engine power and help improve fuel use. As more vehicles are built, the demand for these systems increases. According to CAAM, 31.436 million vehicles were sold in China in 2024, showing a strong market for car parts like transmissions.

The transmission systems market is growing due to higher fuel efficiency needs and electric vehicle expansion. Automakers now use lighter and smarter systems. These help vehicles meet strict fuel rules. For example, the U.S. aims for 50.4 MPG fleet-wide by 2031, as per the Department of Transportation. This directly boosts demand for advanced transmissions.

Moreover, rising EV sales are pushing the need for new transmission designs. These systems must work well with electric drivetrains. Therefore, companies are investing in innovation. In return, this creates fresh opportunities for suppliers who can meet these new technical needs in EV models.

In contrast, mature markets like Europe face tough competition. Many companies already operate there, which limits space for new players. On the flip side, Asia-Pacific offers more room for growth. With China’s rising production, local suppliers have a chance to scale and join the global value chain.

To illustrate the local impact, cities with strong auto industries, like Shanghai or Detroit, gain jobs and investments from growing transmission demand. These areas also attract tech startups and suppliers focused on vehicle components. Hence, the market supports both industrial growth and job creation.

Government support plays a major role in market strength. The U.S. has introduced a $1 billion Drive Forward Fund to help small suppliers shift to EV parts. This initiative, according to the White House, helps keep the auto supply chain stable and modern as vehicles evolve.

Key Takeaways

- The Transmission Systems Market was valued at USD 64.5 billion in 2024 and is expected to reach USD 116.6 billion by 2034, with a CAGR of 6.1%. Growth is driven by increasing demand for automatic transmissions and fuel-efficient systems.

- In 2024, Automatic Transmission led with 38.5%, owing to its convenience, smooth performance, and rising adoption in passenger vehicles.

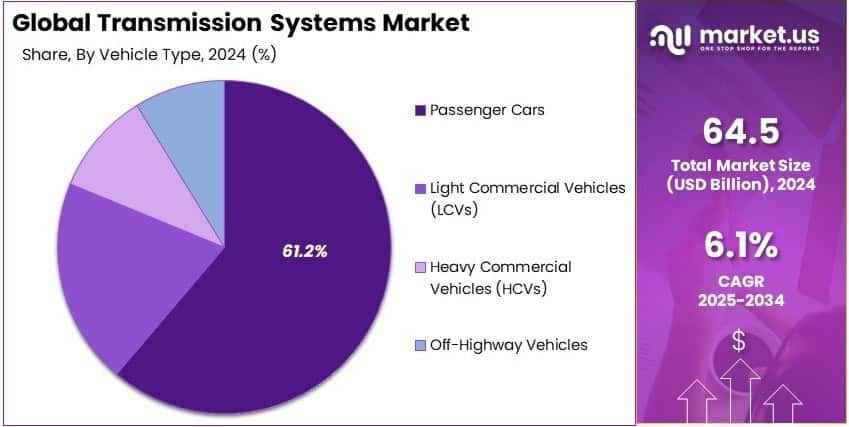

- In 2024, Passenger Cars dominated with 61.2%, driven by increasing urbanization and rising disposable incomes globally.

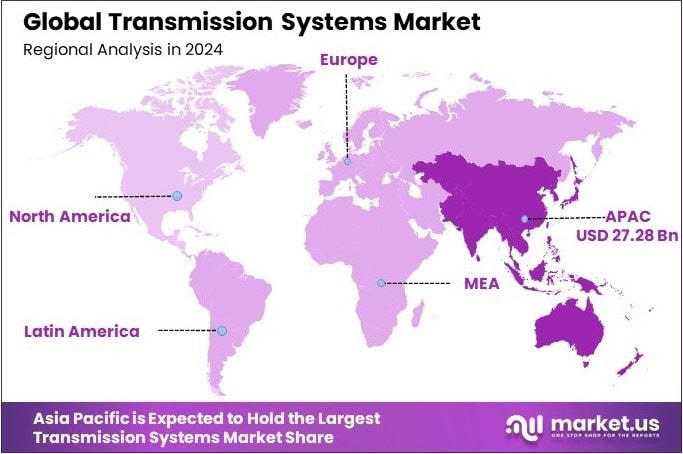

- In 2024, Asia Pacific led with 42.3% with valuation of USD 27.28 billion, fueled by rapid technological advancements and growing automotive sales in China, Japan, and India.

Transmission Type Analysis

Automatic Transmission dominates with 38.5% due to its ease of use and consumer preference for convenience.

In the transmission systems market, the Automatic Transmission segment holds a significant position with a 38.5% market share, primarily because of its convenience and ease of use, which appeals to a broad consumer base globally. This type of transmission simplifies driving by eliminating the need for manual gear changes, which is especially appealing in urban areas with frequent stop-and-go traffic.

The Manual Transmission, known for its control and efficiency, remains popular in certain regions and among enthusiasts who prefer a more engaged driving experience. However, its market share is gradually declining as automatic systems become more advanced and accessible.

Automated Manual Transmission (AMT) offers a compromise between manual and automatic, providing efficiency with automatic gear shifting. It’s particularly favored in budget-friendly and commercial vehicles due to its cost-effectiveness and fuel efficiency.

Continuously Variable Transmission (CVT) is appreciated for its smooth driving experience and fuel efficiency. It’s becoming more common in compact and mid-size cars due to its ability to optimize engine performance and reduce fuel consumption.

Dual-Clutch Transmission (DCT) provides rapid gear shifts and high efficiency, making it popular in sports and performance vehicles. This technology combines the convenience of automatic with the efficiency of manual transmissions, appealing to drivers who seek performance without compromising on comfort.

Vehicle Type Analysis

Passenger Cars dominate with 61.2% due to their vast consumer base and global sales volumes.

The Passenger Cars segment leads the transmission systems market with a 61.2% share, driven by high global sales volumes and the wide range of transmission types available, catering to diverse consumer preferences and needs.

Light Commercial Vehicles (LCVs) are essential in urban setups for businesses and small-scale logistics, contributing significantly to the market with their varied needs for robust and efficient transmission systems. The rise in e-commerce and urbanization has particularly spurred demand for these vehicles.

Heavy Commercial Vehicles (HCVs) are crucial for transport and heavy-duty tasks. The segment’s demand for reliable and strong transmission systems underscores its role in supporting industrial and commercial activities, especially in emerging economies where infrastructure development is ongoing.

Off-Highway Vehicles require specialized transmission systems to handle tough terrains and heavy loads, common in agriculture and construction industries. Their unique requirements drive innovation and adaptation in transmission technologies, supporting the segment’s growth in niche markets.

Key Market Segments

By Transmission Type

- Manual Transmission

- Automatic Transmission

- Automated Manual Transmission (AMT)

- Continuously Variable Transmission (CVT)

- Dual-Clutch Transmission (DCT)

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Off-Highway Vehicles

Driving Factors

Comfort, Technology, and Production Growth Drives Market Expansion

The transmission systems market is witnessing notable growth, mainly due to rising demand for advanced gear-shifting solutions. A key factor is the growing preference for automatic and dual-clutch transmission systems. These technologies enhance driving comfort and reduce the strain of manual gear shifts, especially in urban traffic conditions. Consumers are now more inclined toward vehicles that offer smoother performance and fuel efficiency.

Increasing vehicle production in emerging economies such as India, Brazil, and Southeast Asia is also contributing to this growth. These regions are experiencing a surge in automobile ownership, supported by economic development and expanding middle-class populations. As manufacturing scales up, the demand for reliable and efficient transmission systems grows with it.

Driver comfort and gear shift efficiency have become key priorities for automakers. New transmission models are being developed to provide seamless acceleration and reduced engine load. This focus is influencing product design and performance expectations.

Furthermore, the growth in aftermarket services and retrofit solutions is adding another layer of demand. Vehicle owners are seeking upgrades or replacements for aging transmissions. This creates opportunities for transmission manufacturers to supply both OEMs and the replacement market, fueling further expansion across both new and used vehicle segments.

Restraining Factors

Maintenance and Complexity Restraints Market Progress

Despite ongoing innovation, several challenges are holding back faster growth in the transmission systems market. One of the primary restraints is the high maintenance cost associated with modern transmission systems. Dual-clutch and automatic transmissions, while efficient, are expensive to repair or replace. For many users, particularly in developing markets, this raises long-term ownership costs.

Another concern is the technological complexity of these systems. As transmissions become more electronically controlled, they are harder for traditional mechanics and do-it-yourself (DIY) users to service. This limits widespread adoption, especially in regions where vehicle maintenance is done informally or with limited access to trained technicians.

In certain markets, such as parts of Europe, Africa, and South Asia, manual transmissions still dominate due to cultural preferences and cost sensitivity. As a result, the demand for automatic systems remains lower in these regions, limiting overall market penetration.

Environmental regulations also play a role. Restrictions on traditional transmission fluids due to emissions and environmental concerns are pushing manufacturers to invest in alternative formulations. This transition requires research and adaptation, increasing development costs and complicating supply chains. Collectively, these factors pose a challenge to market players trying to scale up or enter new territories with advanced transmission offerings.

Growth Opportunities

Innovation and Electrification Provides Opportunities

Several emerging trends and innovations are opening new growth opportunities for the transmission systems market. One promising area is the advancement of Continuously Variable Transmission (CVT) technology, especially for compact and fuel-efficient cars. CVTs allow smooth acceleration without fixed gear ratios, which improves fuel economy and driving experience. This appeals to eco-conscious consumers and urban drivers alike.

Another major opportunity lies in integrating AI-based gear shift systems. Artificial intelligence enables real-time analysis of driving behavior and road conditions, allowing the transmission to optimize gear changes for performance and efficiency. Automakers are actively exploring these systems to differentiate their offerings and enhance safety features.

There is also a surge in demand for transmission control units (TCUs) in electric vehicles. Although EVs do not use traditional gearboxes, they still require precise torque management and control systems. TCUs are becoming vital in managing the powertrain response, battery efficiency, and driving dynamics in electric mobility.

Additionally, expansion in autonomous vehicle development is creating new needs for powertrain architecture. These vehicles demand transmission systems that can respond automatically to varying speeds and conditions without human input. Manufacturers investing in such capabilities are well-positioned to lead the future of mobility.

Emerging Trends

Advanced Designs and Connectivity Are Latest Trending Factor

The transmission systems market is evolving quickly due to several trending developments. One of the most impactful is the adoption of lightweight composite materials in transmission housings. These materials reduce overall vehicle weight and improve fuel economy without compromising strength. This trend aligns with automakers’ goals to meet emissions targets and boost performance.

Another noticeable trend is the rise of 8-speed and higher transmission configurations. More gear options help maintain engine efficiency at different speeds, resulting in better acceleration and fuel savings. Luxury and performance car segments are especially driving this demand, setting new benchmarks for transmission systems.

The integration of transmissions with vehicle telematics and connectivity platforms is also shaping the market. Modern vehicles increasingly rely on software to monitor system health, fuel use, and gear performance. This data is shared with drivers and service centers in real-time, enabling predictive maintenance and improved customer experience.

Electrification of transmission components, particularly for hybrid vehicles, is also gaining traction. As hybrid vehicles rely on a mix of electric and traditional drivetrains, transmission systems must adapt to manage energy flow efficiently. These innovations indicate a shift toward smarter, connected, and cleaner transmission solutions for future mobility needs.

Regional Analysis

Asia Pacific Dominates with 42.3% Market Share

Asia Pacific leads the Transmission Systems Market with a 42.3% share, translating to USD 27.28 billion. This dominance is primarily driven by significant investments in infrastructure, rapid industrialization across major economies, and advancements in manufacturing technologies.

The region’s high market share is supported by a growing population and increasing energy demands, coupled with strong governmental support for upgrading and expanding transmission networks. Additionally, the shift towards renewable energy sources in countries like China and India bolsters demand for robust transmission systems.

Looking forward, Asia Pacific’s influence on the global Transmission Systems Market is expected to strengthen. Continued industrial growth and infrastructural developments are likely to further drive the market, with an increasing focus on sustainability and energy efficiency playing a pivotal role.

Regional Mentions:

- North America: North America holds a market share of 24.5% in the Transmission Systems Market, valued at USD 16.9 billion. The region’s market strength is boosted by modernization of aging infrastructure and increasing adoption of smart grids and renewable energy sources.

- Europe: Europe accounts for a 20.1% market share, with a valuation of USD 13.86 billion. The region’s focus on integrating renewable energy sources and enhancing grid reliability underpins its substantial market presence.

- Middle East & Africa: With a market share of 8.2%, valued at USD 5.64 billion, the Middle East & Africa are enhancing their transmission systems to support economic diversification and improve access to electricity across rural areas.

- Latin America: Latin America, holding a 4.9% market share at USD 3.38 billion, is witnessing growth in the Transmission Systems Market through investments in grid interconnectivity and renewable energy projects to tackle its energy demand challenges.

Key Regions and Countries Covered in the Report

- North America

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The Transmission Systems Market is led by major players such as AISIN CORPORATION, ZF Friedrichshafen AG, Allison Transmission, Inc., and BorgWarner Inc. These companies play a crucial role in driving innovation and setting industry standards.

These firms dominate due to their wide product range, covering manual, automatic, and electric transmissions. AISIN and ZF are key suppliers to global car manufacturers, known for precision-engineered systems that improve fuel economy and performance. Allison Transmission leads in commercial vehicle solutions, especially for heavy-duty and defense applications, while BorgWarner is recognized for its focus on hybrid and electric drivetrains.

R&D investment is a shared priority. These companies continually develop smart, electronically controlled transmission systems to meet new regulations and customer demands. Electrification is a growing trend, and these key players are adapting quickly by launching next-generation e-transmissions for hybrid and electric vehicles.

Geographic reach and strong OEM partnerships give them a stable market position. ZF and AISIN have a widespread presence in Asia, Europe, and North America, while BorgWarner and Allison are strongly positioned in the U.S. commercial and off-highway markets.

As global demand shifts towards efficient and eco-friendly drivetrains, these top companies are focusing on lightweight materials, system integration, and energy-saving technologies. Their leadership is expected to remain strong as the transition to electric mobility continues.

Major Companies in the Market

- AISIN CORPORATION

- Allison Transmission, Inc.

- BorgWarner Inc.

- Continental AG

- Eaton Corporation PLC

- GKN Automotive Limited

- JATCO Ltd.

- Magna International Inc.

- Schaeffler AG

- ZF Friedrichshafen AG

Recent Developments

- Schaeffler AG Merges with Vitesco Technologies Group AG: On October 2024, Schaeffler AG and Vitesco Technologies Group AG completed their merger, forming a leading motion technology company. The consolidation enhances capabilities in powertrain and chassis systems, reinforcing their position in the evolving automotive market.

- Cadence Design Systems Acquires BETA CAE Systems: In June 2024, Cadence Design Systems completed its acquisition of BETA CAE Systems, a provider of simulation and analysis software. With BETA CAE generating $90 million in annual revenue, Cadence expects the acquisition to contribute $40 million to 2024 revenue and become accretive to earnings by 2025.

Report Scope

link

– First Classic Car Auctions of the Year")