Europe Automotive Brake System Market Size and Share, 2034

Europe Automotive Brake System Market Report Summary

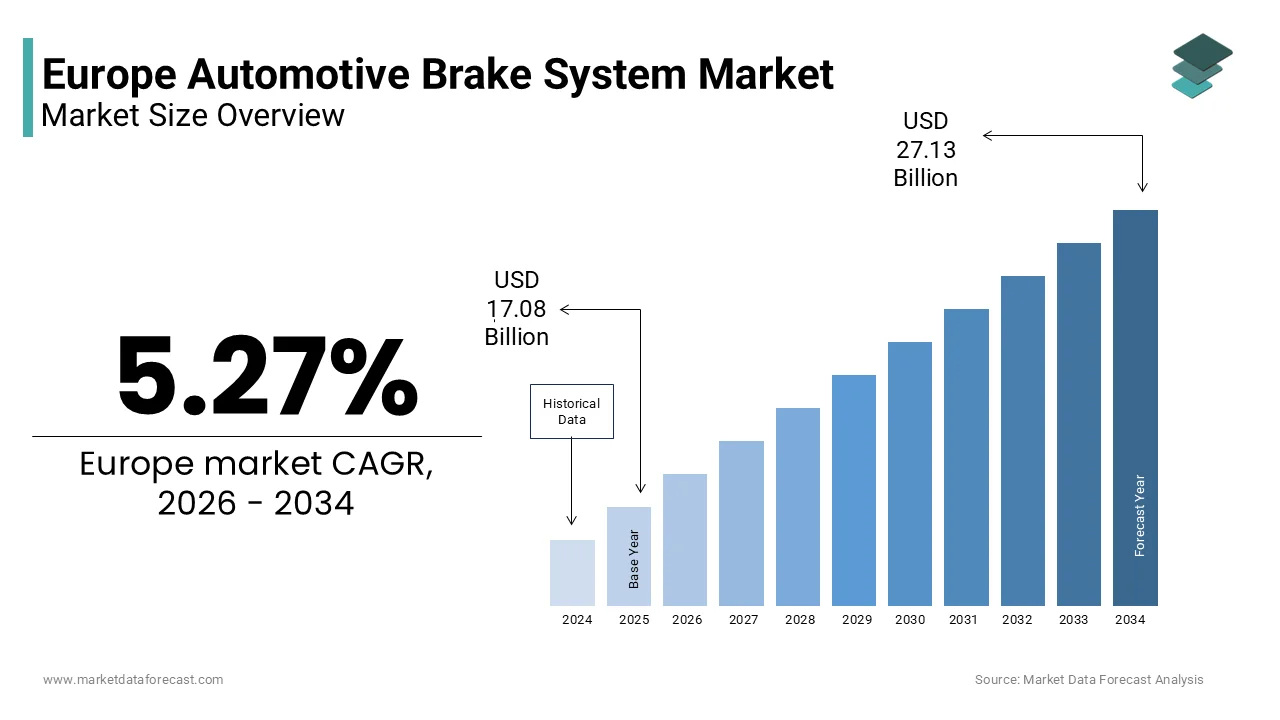

The Europe automotive brake system market was valued at USD 17.08 billion in 2025 and is estimated to reach USD 17.98 billion in 2026, with the market projected to grow to USD 27.13 billion by 2034, registering a CAGR of 5.27 percent during the forecast period. Market growth is driven by rising vehicle production, increasing focus on road safety regulations, and growing adoption of advanced braking technologies across passenger and commercial vehicles. The shift toward electric and hybrid vehicles, along with continuous advancements in braking performance, durability, and electronic integration, is further supporting market expansion across Europe.

Key Market Trends

- Increasing adoption of disc brake systems due to superior braking performance, heat dissipation, and durability.

- Rising demand for advanced braking technologies such as anti lock braking systems and electronic stability control.

- Growing emphasis on vehicle safety standards and regulatory compliance across European countries.

- Expansion of electric and hybrid vehicle production driving innovation in lightweight and regenerative braking systems.

- Strong aftermarket demand supported by high vehicle parc and regular maintenance requirements.

Segmental Insights

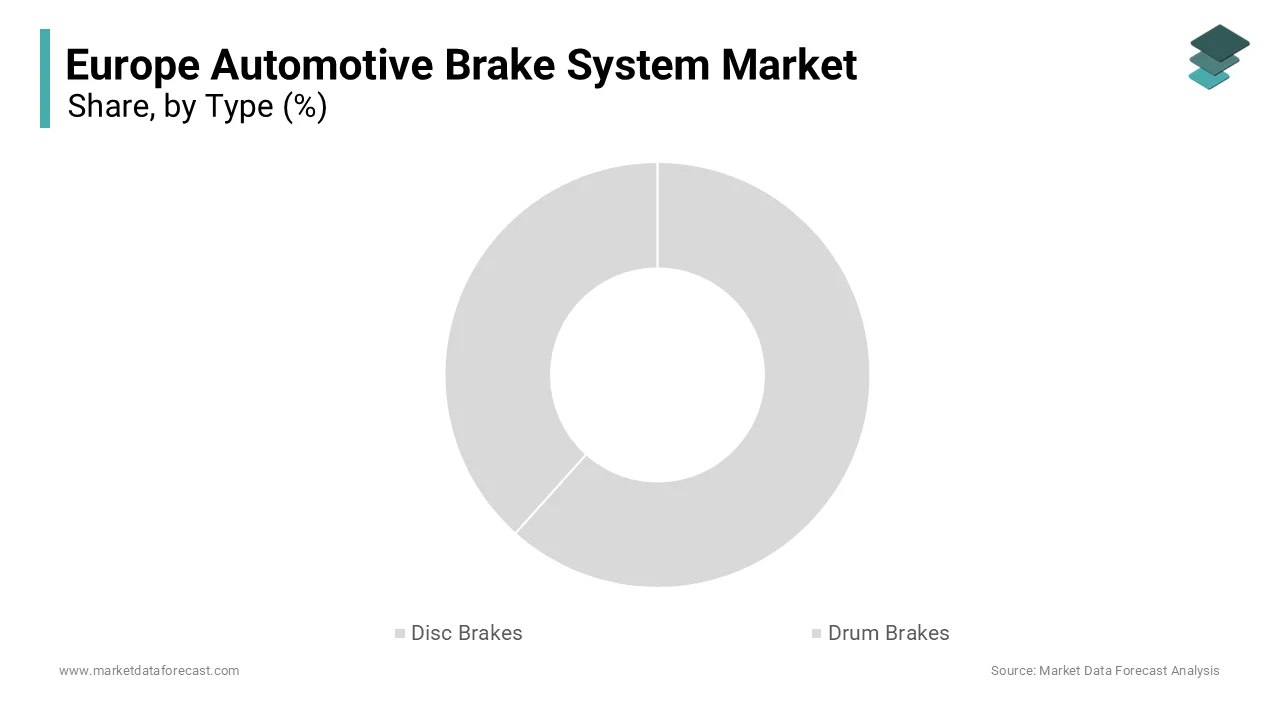

- Based on type, the disc brake segment dominated the Europe automotive brake system market by accounting for 77.4 percent of the regional market share in 2025. This dominance is attributed to the widespread use of disc brakes in modern passenger cars and premium vehicles due to their consistent performance and enhanced safety benefits.

- Based on vehicle type, the passenger cars segment led the market by capturing 66.5 percent of the European market share in 2025. Growth in this segment is supported by high passenger vehicle ownership, rising urbanization, and increasing consumer awareness of vehicle safety features.

Regional Insights

- Germany held the leading position in the Europe automotive brake system market, accounting for 25.4 percent of the regional market share in 2025. The country’s dominance is driven by its strong automotive manufacturing base, presence of major original equipment manufacturers, and continuous investments in vehicle safety and innovation.

- Other European countries continue to contribute significantly, supported by steady vehicle production, growing electric vehicle adoption, and strong aftermarket demand.

Competitive Landscape

The Europe automotive brake system market is moderately consolidated, with global and regional players competing based on technology, product reliability, and long term partnerships with automotive manufacturers. Leading companies are focusing on research and development, lightweight materials, and integration of electronic braking systems to enhance safety and performance. Strategic collaborations with vehicle manufacturers and expansion of aftermarket networks remain key growth strategies. Prominent players operating in the market include Aisin, Akebono Brake Industry, Brembo, Continental, Hitachi Astemo, Knorr Bremse, Robert Bosch, Textar, Valeo, and ZF Friedrichshafen.

Europe Automotive Brake System Market Size

The Europe automotive brake system market size was valued at USD 17.08 billion in 2025 and is projected to reach USD 27.13 billion by 2034 from USD 17.98 billion in 2026, growing at a CAGR of 5.27%.

Automotive brake systems encompass a sophisticated suite of mechanical, hydraulic, electronic, and softwareintegrated components engineered to decelerate or halt vehicles safely under diverse driving conditions. These systems include disc and drum brakes, antilock braking systems, electronic stability control, brakebywire architectures, and regenerative braking modules, particularly in electrified powertrains. The European market is distinguished by its rigorous safety mandates, advanced driver assistance integration, and the rapid shift toward electrification, which fundamentally alters braking dynamics and component requirements. According to the European Commission, nearly all new passenger vehicles sold in the European Union in 2023 were equipped with mandatory electronic stability control and antilock braking systems as stipulated under UN Regulation No. 13H. Furthermore, according to the European Environment Agency, the average age of the EU lightduty vehicle fleet exceeded 12 years in 2023, intensifying demand for replacement brake components that meet modern performance and emissions standards. As per Eurostat, road transport accounted for about 71% of total EU transportrelated final energy consumption in 2022, placing efficiency and safety at the core of regulatory and consumer priorities. This evolving technical and regulatory landscape positions the automotive brake system not merely as a safety device but as a critical node in the broader mobility ecosystem.

MARKET DRIVERS

Mandatory Advanced Driver Assistance Systems Accelerate Adoption

The phased enforcement of General Safety Regulation (GSR 2) mandates by the European Union has become a primary catalyst for advanced brake system integration across all new vehicle types, which is majorly driving the growth of the European automotive brake system market. Effective from July 2022, the regulation requires autonomous emergency braking (AEB), intelligent speed assistance, and lane keeping assist as standard features for typeapproved vehicles, with full applicability to all new registrations by 2024. According to the European Commission, these systems rely fundamentally on highresponse electrohydraulic or electromechanical brake actuators capable of millisecondlevel intervention without driver input. As per the European Transport Safety Council, AEB can reduce rearend collisions significantly in urban environments, making it a cornerstone of the EU’s Vision Zero road fatality strategy. The regulation further stipulates that AEB must function effectively at speeds up to 60 km/h for cars and 40 km/h for vulnerable road user detection, which is requiring enhanced sensor fusion and brake modulation algorithms. As a result, legacy vacuumassisted hydraulic systems are being rapidly supplanted by brakebywire and electrohydraulic boosters from suppliers like Bosch and Continental. As per the European New Car Assessment Programme (Euro NCAP), maximum safety ratings are awarded only to vehicles demonstrating robust AEB performance under diverse conditions, reinforcing OEM investment in nextgeneration braking hardware.

Rise of Electric and Hybrid Vehicles Transforms Braking Architecture

The accelerating electrification of Europe’s vehicle fleet is fundamentally reshaping brake system design through the imperative of regenerative braking integration, which is further contributing to the expansion of the European automotive brake system market. Unlike internal combustion engine vehicles, electric and hybrid models recover kinetic energy during deceleration using the electric motor, thereby reducing reliance on friction brakes and extending service intervals. However, this necessitates complex coordination between regenerative and mechanical systems to ensure seamless pedal feel and failsafe operation. According to the European Automobile Manufacturers Association (ACEA), electrically chargeable vehicles accounted for about 25% of all new car registrations in the EU in 2023, up from just 3% in 2019. According to the International Energy Agency (IEA), the EU added over 2 million electric passenger cars to its roads in 2023 alone, amplifying demand for integrated braking solutions. Moreover, regenerative braking reduces particulate matter emissions from brake wear, a growing environmental concern. As per the European Environment Agency, nonexhaust emissions including brake dust contributed to more than half of road transportrelated PM2.5 in 2022, prompting the EU to propose stricter limits under the upcoming Euro 7 standards. Consequently, manufacturers are investing in lowwear pad materials and predictive braking algorithms that maximize energy recovery while minimizing particulate release.

MARKET RESTRAINTS

Stringent Emission and Particulate Regulations Increase Compliance Costs

The EU’s proposed Euro 7 emission standards, scheduled for implementation in 2025, introduce unprecedented constraints on nonexhaust emissions including brake particulate matter, which is hindering the European automotive brake system market growth. Unlike previous norms that focused solely on tailpipe pollutants, Euro 7 sets a limit of 7 mg/km for brake wear particles in passenger cars. According to the European Commission’s regulatory proposal, this threshold requires reformulation of friction materials, adoption of encapsulated calipers, and integration of active dust suppression technologies—all of which elevate production costs. As per the European Council for Motor Trades and Repairs, compliance with these new particulate limits could increase the cost of a standard brake pad set substantially due to the use of copperfree ceramic composites and specialized coatings. Furthermore, testing protocols mandate realworld driving emissions (RDE) style assessment using portable particulate measurement systems, adding complexity to homologation. According to the European Automobile Manufacturers Association (ACEA), small and medium suppliers may lack the capital to retool production lines for lowdust formulations, potentially disrupting supply continuity. Larger players like Brembo and Akebono are piloting ventilated disc and regenerative synergy systems, but the fragmented supplier base across Southern and Eastern Europe faces steep adaptation barriers.

Supply Chain Fragmentation for Critical Raw Materials

Europe’s automotive brake system market faces mounting vulnerability due to dependence on geopolitically concentrated sources for essential raw materials including copper, antimony, and rare earth elements used in friction compounds and electronic control units. According to the European Raw Materials Alliance, the EU imports over 70% of its annual copper consumption. As per the United States Geological Survey, Chinese production accounts for nearly 80% of global antimony supply. This concentration creates exposure to export restrictions, price volatility, and logistical disruptions as evidenced during the 2022 energy crisis when European copper premiums surged. The EU’s Critical Raw Materials Act identifies antimony and copper as strategic materials, but domestic recycling rates remain low. According to the European Recycling Platform, less than 35% of endoflife brake components are recovered for reuse. Moreover, the shift toward lowcopper and copperfree formulations to meet environmental standards has intensified competition for alternative materials like aramid fibers and ceramics, whose supply chains are still nascent in Europe. Without diversified sourcing or circular economy infrastructure, brake system manufacturers risk production delays, cost inflation, and reduced design flexibility.

MARKET OPPORTUNITIES

Integration of Brake Systems with Vehicle to Everything Networks

The emergence of cooperative intelligent transport systems (CITS) across Europe presents a transformative opportunity for the European automotive brake system market. Under the EU’s Delegated Act on Connected and Automated Mobility, vehicles equipped with V2X communication can receive advance warnings about hazards, congestion, or emergency braking events ahead, which is enabling predictive brake actuation before the driver perceives a threat. According to the European Commission, over 15,000 kilometers of EU road corridors are slated for CITS deployment by 2027 under the Connecting Europe Facility program, creating a live data ecosystem for proactive safety interventions. This environment favors brake systems with ultrafast response electrohydraulic boosters and overtheair updatecapable electronic control units that can adapt braking logic based on external inputs. As per pilot projects in Germany and the Netherlands validated by the German Aerospace Center (DLR), V2Xenabled emergency braking can reduce collision severity by up to 50% in highway platooning scenarios. Furthermore, the upcoming UNECE Regulation 157 on Automated Lane Keeping Systems mandates failoperational braking for Level 3 autonomy, requiring redundant actuation pathways that integrate seamlessly with V2X alerts. Companies like Continental and ZF are already developing brake control units with embedded 5G and CV2X modems, positioning them to capitalize on this convergence of connectivity and active safety. As European cities adopt smart traffic management platforms, brake systems will evolve from reactive components to anticipatory safety agents within a distributed mobility network.

Aftermarket Modernization Through Digital Diagnostics and Telematics

The digitization of vehicle maintenance ecosystems offers a significant growth vector for the European automotive brake system market. Modern European vehicles increasingly transmit realtime brake wear data, tire pressure, and fluid levels to cloud platforms, enabling service providers to schedule interventions before failures occur. According to the European Association of Automotive Suppliers, over 60% of new passenger cars sold in the EU in 2023 featured embedded telematics capable of monitoring brake pad thickness and rotor condition through acoustic or position sensors. This data stream supports subscriptionbased maintenance models and enhances customer retention for OEMs and authorized workshops. In parallel, independent repair networks are adopting AIpowered diagnostic tools like those from Bosch Automotive Aftermarket, which analyze OBD2 signals to estimate remaining brake life with 90% accuracy as verified by TÜV Rheinland trials. The European Commission’s Right to Repair initiative further mandates standardized access to this data by 2026, ensuring a level playing field for aftermarket participants. Consequently, there is rising demand for brake components with integrated wear indicators, smart calipers, and RFIDtagged parts traceable through blockchain ledgers. Companies such as TRW and Bendix are embedding microsensors into pads and discs to feed digital twins of vehicle systems, enabling dynamic calibration of brake force distribution. This fusion of hardware intelligence and service digitization transforms the brake system from a consumable into a connected service enabler with recurring revenue potential across the vehicle lifecycle.

MARKET CHALLENGES

Thermal Management Limitations in High Performance Applications

Highperformance and heavyduty vehicles operating in Europe’s mountainous and highspeed environments face severe thermal challenges that compromise brake system reliability and safety, which is challenging the growth of the European automotive brake system market. Repeated hard braking, especially on Alpine descents or Autobahn sections, generates extreme temperatures exceeding 600°C at the discpad interface, leading to brake fade, fluid vaporization, and structural fatigue. According to the German Federal Highway Research Institute (BASt), prolonged downhill braking on gradients above 6% can reduce stopping power by up to 40% in conventional systems lacking active cooling. While carbonceramic discs offer superior heat resistance, their adoption remains limited to premium segments due to costs exceeding €10,000 per axle as reported by the European Automotive Task Force. Most massmarket vehicles still rely on castiron rotors, which suffer from thermal cracking and warping under sustained load. The European New Car Assessment Programme has begun evaluating brake performance under repeated stress tests, yet no harmonized standard exists for thermal endurance across commercial or passenger categories. Moreover, the shift to regenerative braking in electric SUVs reduces mechanical brake usage, leading to corrosion and uneven pad deposits during cold stops, which is a phenomenon documented in 28% of EV inspections by DEKRA in 2023. Until costeffective thermal barrier coatings, active air ducting, or phasechange materials achieve scale, these limitations will persist as a critical engineering bottleneck, particularly for fleet and emergency service vehicles operating in demanding terrains.

Cybersecurity Vulnerabilities in Electronically Controlled Braking

The increasing reliance on softwaredefined brakebywire and electrohydraulic systems introduces unprecedented cybersecurity risks that threaten vehicle safety and regulatory compliance, which is further challenging the regional market expansion. Unlike traditional hydraulic systems, modern brake architectures depend on CAN bus and Ethernet networks to transmit pedal commands from sensors to actuators, creating potential entry points for malicious actors. According to the European Union Agency for Cybersecurity (ENISA), over 40% of automotive cyber incidents reported in 2023 involved manipulation of chassis control systems including braking and steering. A compromised brake control unit could theoretically disable deceleration, override pedal input, or trigger false emergency stops with catastrophic consequences. The upcoming UNECE Regulation 155 mandates robust cybersecurity management systems for all new vehicle types, but implementation varies widely among suppliers. As per penetration tests conducted by KPMG in 2024, 30% of thirdparty brake ECUs in European supply chains lacked secure boot or encrypted firmware updates, leaving them susceptible to code injection attacks. Moreover, overtheair update capabilities, while beneficial for bug fixes, also expand the attack surface if not protected by hardware security modules. The European Commission’s Automotive Cybersecurity Guidelines require intrusion detection systems in critical domains, yet integration with brake ECUs remains inconsistent due to legacy architectures and cost constraints. Until endtoend security from silicon to software becomes standard practice, the transition to fully electronic braking will remain constrained by trust and liability concerns among regulators, insurers, and consumers alike.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.27% |

|

Segments Covered |

By Type, Vehicle Type, Technology, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Aisin, Akebono Brake Industry, Brembo, Continental, Hitachi Astemo, Knorr Bremse, Robert Bosch, Textar, Valeo, and ZF Friedrichshafen |

SEGMENTAL ANALYSIS

By Type Insights

The disc brake segment dominated the Europe automotive brake system market by accounting for 77.4% of the regional market share in 2025. The dominance of disc brake segment in this regional market is driven by the superior thermal performance, consistent stopping power, and compatibility with advanced safety systems such as antilock braking and electronic stability control as technologies mandated across the European Union. Unlike drum brakes, disc systems dissipate heat more efficiently, reducing the risk of fade during repeated or highspeed deceleration, a critical requirement on Europe’s extensive highway networks including the German Autobahn and French autoroutes. According to the European Commission, all new passenger vehicles typeapproved after 2004 must feature disc brakes on front axles at minimum, and most now include them on all four wheels to meet UN Regulation 13H performance thresholds. As per the European New Car Assessment Programme, full disc configurations are incentivized by higher safety ratings awarded to vehicles demonstrating shorter cold and hot stopping distances. According to DEKRA, over 92% of new cars registered in Germany, Italy, and Sweden in 2023 were equipped with fourwheel disc brakes, reflecting consumer and OEM preference for enhanced control. Additionally, the rise of heavier electric vehicles has accelerated adoption of ventilated and slotted disc variants capable of managing elevated kinetic energy loads. As per the International Energy Agency, the average curb weight of new EU passenger cars increased by 11% between 2019 and 2023 due to battery packs and ADAS hardware, making robust disc systems nonnegotiable for safety compliance and driving dynamics.

The disc brake segment is also the fastest growing and is expected to witness a CAGR of .06% over the forecast period owing to the technological evolution beyond basic friction management toward integrated intelligent architectures that support electrification and automation. A major factor is the incompatibility of drum brakes with regenerative braking systems prevalent in hybrid and electric vehicles. Regenerative braking recovers kinetic energy during deceleration but requires precise coordination with mechanical brakes to ensure seamless pedal feel and failsafe operation as coordination only achievable with electronically controlled disc calipers. According to the European Automobile Manufacturers Association, electrically chargeable vehicles represented 25% of all new car registrations in the EU in 2023, and nearly all utilize discbased friction systems paired with electrohydraulic boosters like Bosch iBooster. Furthermore, upcoming Euro 7 emission standards will impose limits on brake particulate matter, prompting innovation in lowdust disc materials such as carbonsilicon carbide composites and encapsulated caliper designs. As per the German Aerospace Center, lowwear disc systems can reduce PM10 emissions from braking by up to 60% compared to conventional castiron setups. With cities like Paris and Amsterdam planning lowemission zones that may eventually restrict highparticulate vehicles, disc brake innovation aligns directly with urban air quality mandates, ensuring sustained demand beyond mere replacement cycles.

By Vehicle Type Insights

The passenger cars segment led the market by commanding for 66.5% of the European market share in 2025. The leading position of passenger cars segment in this regional market is driven by the sheer volume of lightduty vehicle production, registration, and servicing across the region, where personal mobility remains deeply embedded in transportation culture despite urban densification efforts. According to Eurostat, over 13.2 million new passenger cars were registered in the European Union in 2023, each requiring a complete brake system compliant with stringent safety norms. As per the European Environment Agency, the average age of the EU passenger car fleet exceeded 12 years in 2023, creating a vast installed base in need of periodic component replacement. Unlike commercial fleets, which follow structured maintenance schedules, private vehicle owners often delay servicing until performance degrades, leading to higher pervehicle replacement frequency. Moreover, passenger cars are early adopters of advanced braking technologies including automatic emergency braking and brake assist features mandated under the EU General Safety Regulation. According to the European Transport Safety Council, AEB systems are now standard on 98% of new EU passenger models, necessitating highprecision disc brakes with rapidresponse calipers and redundant sensors. This regulatory and demographic confluence ensures consistent highvolume demand for both original equipment and aftermarket brake systems tailored to diverse driving conditions from Nordic winters to Mediterranean mountain passes.

The commercial vehicles segment is the fastest growing and is anticipated to register a CAGR of 6.3% over the forecast period due to the logistics expansion, infrastructure investment, and evolving safety mandates specific to heavy transport. Europe’s ecommerce boom has dramatically increased freight volumes. According to the European Commission, light commercial vehicle kilometers travelled rose by 22% between 2020 and 2023. This intensifies wear on braking components, particularly in stopandgo urban delivery cycles where drum brakes on rear axles remain common but are increasingly supplemented with auxiliary retarders and disc upgrades for safety. More significantly, the revised EU General Safety Regulation effective 2024 mandates advanced emergency braking for all new trucks and buses capable of detecting both vehicles and vulnerable road users—a requirement impossible to fulfill with legacy drum systems alone. As per the European Road Safety Observatory, heavy goods vehicles were involved in 16% of all road fatalities in the EU in 2022 despite representing only 5% of traffic, prompting stricter technical oversight. Manufacturers like DAF and Scania now equip new trucks with full air disc brake systems offering 30% shorter stopping distances, according to TÜV SÜD validation tests. Additionally, the European Green Deal’s push for zeroemission urban logistics has accelerated adoption of electric vans from MercedesBenz and Renault, which rely on disc brakes for regenerative integration and thermal resilience. These converging forces position commercial vehicles as the highest growth vector for advanced brake system deployment in Europe.

REGIONAL ANALYSIS

Germany Automotive Brake System Market Analysis

Germany held the leading position in the European automotive brake system market and captured 25.4% of the regional market share in 2025. The leading position of Germany in the European automotive brake system market is driven by its status as a global automotive engineering hub and home to premium OEMs including BMW, MercedesBenz, and Volkswagen. The country’s emphasis on highspeed driving performance and safety rigor translates into demand for highperformance ventilated disc brakes and electromechanical actuation systems. According to the German Federal Motor Transport Authority, over 2.8 million new passenger cars were registered in Germany in 2023, with more than 85% featuring fourwheel disc brakes and advanced driver assistance integration. The nation’s Autobahn network, where speed limits are partially absent, necessitates exceptional thermal resilience in braking components, elevating specifications beyond EU minimums. Furthermore, Germany hosts Tier 1 suppliers like Continental and Bosch, whose R&D centers continuously refine brakebywire and redundancy architectures for Level 3 autonomy. As per the Fraunhofer Institute for Structural Durability, German OEMs allocate 12–15% of chassis development budgets to brake system innovation, reflecting its strategic importance. With stringent TÜV inspection protocols requiring measurable pad thickness and rotor integrity every two years, the aftermarket remains robust, ensuring sustained demand across both original and replacement channels.

France Automotive Brake System Market Analysis

France captured a promising share of the European automotive brake system market in 2025. The growth of France in the European market is attributed to the strong domestic manufacturing presence and proactive road safety policies. The country is home to Stellantis, which produces Peugeot, Citroën, and DS models widely sold across Southern and Eastern Europe, creating consistent OE demand for costoptimized yet compliant brake systems. According to France’s Ministry of Ecological Transition, over 1.9 million new passenger vehicles were registered in 2023, with mandatory inclusion of autonomous emergency braking under national implementation of EU GSR 2 rules. Urban congestion in cities like Paris, Lyon, and Marseille has intensified wear on braking components, particularly in delivery and taxi fleets, prompting faster replacement cycles. As per Sécurité Routière, brakerelated defects were cited in 9% of vehicle failures during mandatory technical inspections in 2023, underscoring maintenance vigilance. Moreover, France enforces strict noise and particulate limits in lowemission zones, with Paris targeting a ban on internal combustion vehicles by 2030, accelerating adoption of lowdust ceramic brake pads. The government’s “Plan de Relance” also allocated funding for retrofitting municipal bus fleets with air disc brakes, enhancing commercial segment activity.

United Kingdom Automotive Brake System Market Analysis

The UK is expected to hold a prominent share of the European automotive brake system market during the forecast period owing to the postBrexit regulatory continuity and a mature vehicle parc requiring extensive servicing. Despite leaving the EU, the UK retained Ecodesign and General Safety Regulation standards through the GB Type Approval framework, ensuring ongoing alignment with continental technical requirements. According to the Society of Motor Manufacturers and Traders, 1.8 million new cars were registered in the UK in 2023, nearly all equipped with disc brakes and AEB as standard. The country’s extensive rural and hilly terrain, particularly in Wales and Scotland, increases brake load severity, promoting demand for corrosionresistant coated discs and highfriction pads. As per the Driver and Vehicle Standards Agency, braking efficiency was the second most common reason for MOT test failures, accounting for 14% of rejections in 2023, highlighting active aftermarket engagement. Additionally, the UK’s commitment to phasing out new petrol and diesel car sales by 2030 has accelerated electric vehicle adoption, with models like the Nissan Leaf and Tesla Model Y relying exclusively on discbased friction systems for failsafe backup. Companies like AP Racing, headquartered in the West Midlands, continue to supply highperformance braking solutions to motorsport and premium segments, reinforcing engineering depth.

Italy Automotive Brake System Market Analysis

Italy is predicted to register a healthy CAGR in the European automotive brake system market over the forecast period owing to its dense urban fabric, aging vehicle fleet, and vibrant motorsport heritage. According to ISTAT, the National Institute of Statistics, the average age of Italy’s passenger car fleet reached 13.2 years in 2023, making it one of the oldest in Europe and driving high replacement rates for brake pads, rotors, and fluid. Narrow historic streets in cities like Rome, Florence, and Naples necessitate frequent lowspeed braking, accelerating component wear, particularly in manual transmission vehicles, which still represent over 60% of the parc as per ANFIA data. Moreover, Italy’s southern regions experience high ambient temperatures, which degrade brake fluid performance and increase fade risk, prompting demand for DOT 4 and DOT 5.1 formulations with higher wet boiling points. As per the Italian Ministry of Infrastructure, over 40% of roadside vehicle checks in 2023 identified deficient braking systems, leading to fines and mandatory repairs. On the innovation front, Italian OEMs like Ferrari, Lamborghini, and Maserati collaborate with Brembo to develop carbonceramic disc systems that filter down to highperformance road cars. Brembo itself supplies braking components to over 20 global automakers, with its Bergamo facility serving as a key European hub.

Spain Automotive Brake System Market Analysis

Spain is projected to grow at a steady CAGR in the European automotive brake system market during the forecast period. The role of Spain as a major automotive manufacturing base and tourismdriven vehicle usage patterns are propelling the Spanish market growth. According to ANFAC, the Spanish Association of Car and Truck Manufacturers, Spain is the EU’s secondlargest car producer after Germany, with factories operated by SEAT, Stellantis, and Ford assembling over 2.4 million vehicles in 2023. These plants generate substantial original equipment demand for standardized yet durable brake systems suited to Mediterranean climate conditions. Coastal and island regions, including the Balearics and Canary Islands, experience high humidity and salt exposure, accelerating corrosion of uncoated steel components, thus favoring galvanized or aluminum hat disc assemblies. Furthermore, Spain’s extensive highway network connecting Madrid, Barcelona, and Valencia sees significant longdistance travel, increasing thermal stress on brakes during mountain descents in regions like the Pyrenees and Sierra Nevada. As per the Directorate General of Traffic, brake failure contributed to 7% of fatal accidents on interurban roads in 2023, prompting public awareness campaigns and stricter inspection criteria. The government’s Moves III plan also subsidizes electric van adoption for lastmile delivery, with models like the Citroën ëBerlingo requiring disc brakes compatible with regenerative coordination.

COMPETITIVE LANDSCAPE

Competition in the Europe automotive brake system market is characterized by intense technological differentiation stringent regulatory alignment and deep OEM integration. Established players leverage decades of engineering expertise in friction dynamics thermal management and electronic control to deliver systems that meet both safety mandates and performance expectations. The market is not price driven but rather defined by precision reliability and compatibility with advanced driver assistance and electrified powertrains. Incumbents face pressure from emerging suppliers offering cost competitive alternatives particularly in the aftermarket and commercial segments yet struggle to match the validation depth and system integration capabilities of Tier 1 leaders. Regulatory shifts notably Euro 7 particulate limits and GSR 2 safety mandates raise entry barriers favoring firms with robust R and D infrastructure. Consolidation is ongoing as companies acquire software and sensor specialists to build end to end braking ecosystems. Innovation velocity in areas like brake by wire regenerative coordination and V2X enabled intervention now determines market leadership more than production scale alone. The result is a dynamic oligopolistic structure where technical excellence and regulatory foresight outweigh volume advantages.

KEY MARKET PLAYERS

Some of the notable key players in the Europe automotive brake system market are

- Aisin

- Akebono Brake Industry

- Brembo

- Continental

- Hitachi Astemo

- Knorr-Bremse

- Robert Bosch

- Textar

- Valeo

- ZF Friedrichshafen

Top Players in the Market

- Brembo is an Italian engineering leader renowned for high performance braking systems used by premium and motorsport brands globally. The company supplies fixed caliper disc brakes carbon ceramic rotors and electronic brake control modules to manufacturers including Ferrari Lamborghini Porsche and Tesla. Brembo has deep integration across Europe’s automotive value chain with R and D centers in Italy Germany and the UK focused on lightweight materials thermal management and brake by wire technologies. In recent years Brembo accelerated its electrification strategy by launching the Sensify intelligent braking platform which replaces traditional hydraulic circuits with software controlled electro mechanical actuators. This system enables precise regenerative blending and over the air calibration aligning with EU safety and emissions mandates. The company also expanded its Bergamo facility to produce low particulate brake kits compliant with upcoming Euro 7 standards reinforcing its leadership in sustainable high-performance braking.

- Continental is a German automotive technology giant with a comprehensive portfolio spanning hydraulic brake boosters electronic stability control and integrated chassis systems. Its MK C1 brake by wire unit combines booster master cylinder and ESC into a single compact module reducing weight and enabling faster response times critical for autonomous driving. Continental supplies major European OEMs including Volkswagen BMW and Stellantis and has been instrumental in deploying autonomous emergency braking across mass market vehicles. To strengthen its position the company intensified collaboration with semiconductor firms to secure supply of ASICs for brake control units amid global chip shortages. It also launched a predictive maintenance service using vehicle telematics to monitor brake wear and fluid degradation enabling proactive servicing. Furthermore, Continental invested in hydrogen resistant coatings for commercial vehicle brakes supporting zero emission truck deployments in EU urban logistics corridors.

- ZF is a leading German supplier of advanced braking and chassis technologies with global reach across passenger and commercial vehicle segments. The company’s Integrated Brake Control IBC system serves as the foundation for electric and automated vehicles offering high pressure buildup rates and seamless regenerative coordination. ZF supplies brake systems to Volvo Daimler and Rivian and has expanded its electromechanical capabilities through acquisitions in actuator and sensor domains. Recently ZF inaugurated a dedicated e mobility competence center in Koblenz focusing on brake redundancy architectures for Level 3 autonomy. The firm also partnered with European cities to test connected braking that responds to V2X hazard alerts enhancing intersection safety. Additionally, ZF developed low dust brake pads using recycled steel fibers to meet EU particulate limits while maintaining friction stability under wet conditions. These innovations position ZF at the convergence of safety sustainability and digitalization in next generation braking.

Top Strategies Used by the Key Market Participants

Key players in the Europe automotive brake system market pursue multifaceted strategies to sustain competitive advantage. Product innovation centers on developing intelligent brake by wire systems that support electrification autonomy and connectivity. Vertical integration ensures control over critical components like sensors actuators and software stacks reducing dependency on volatile supply chains. Strategic partnerships with OEMs municipalities and tech firms accelerate co development of safety solutions aligned with regulatory timelines. Geographic expansion focuses on Eastern Europe and Southern Mediterranean regions where vehicle parc renewal is accelerating. Sustainability initiatives include low particulate friction materials circular design for remanufacturing and compliance with Euro 7 non-exhaust emission rules. Investment in digital services such as predictive maintenance and over the air updates transforms braking from a hardware product into a lifecycle solution. These approaches collectively enhance technological leadership customer retention and regulatory resilience in a rapidly evolving mobility landscape.

MARKET SEGMENTATION

This research report on the European automotive brake system market has been segmented and sub-segmented based on categories.

By Type

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Technology

- Anti Lock Brake System ABS

- Traction Control System TCS

- Electronic Stability Control ESC

- Electronic Brake Force Distribution EBD

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link

– First Classic Car Auctions of the Year")