Deals are back for car shoppers, but business is still sluggish

St. Louis Park resident Steve Asp had his heart set on leasing a Ford SUV.

But even after his usual dealership offered him thousands off his preferred model, the monthly payment with interest charges was almost $200 more than what he currently pays, so he decided to walk away from the deal and shop around.

The price of cars has started to go down, a relief to shoppers facing the record highs of the past few years. Inventory also is increasing as the country turns a corner from pandemic-fueled supply chain problems.

Some car dealers are even starting to haggle and offer a few discounts. Yet in this slow return to a more normal market, some shoppers remain hesitant to buy as higher auto loan rates and unpredictable economic conditions make them delay big-ticket purchases.

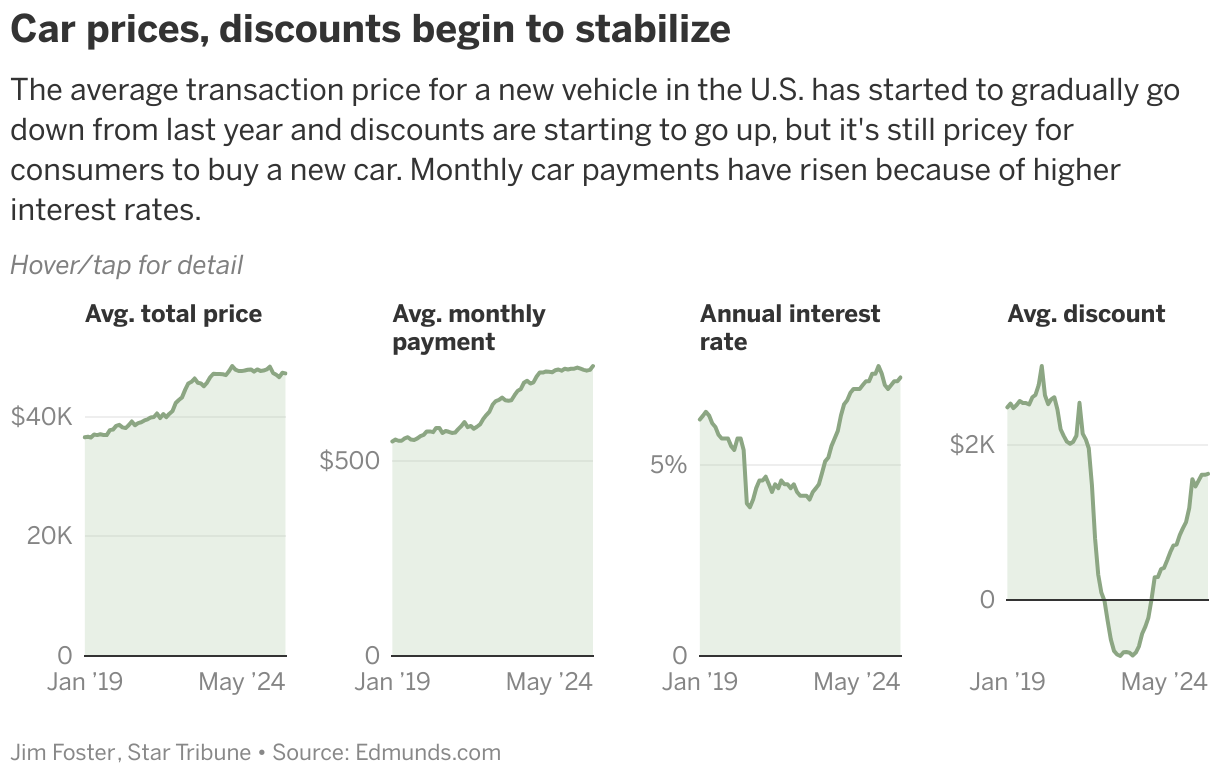

“We are looking at monthly payments over $700 [on average for new cars] and that’s a daunting prospect for so many people,” said Joseph Yoon, a consumer insights analyst at automotive shopping website Edmunds.com.

If they can, many consumers are taking their time to buy a vehicle. Some are waiting to see whether the Federal Reserve cuts interest rates later in the year so the cost of an auto loan goes down. Some are watching to see who wins the presidential election in November, either worried about long-term economic uncertainty or anticipating inflation relief depending on who wins.

Still, economists say other consumers are hesitating because costs have significantly jumped in nearly all aspects of their lives, forcing them to tighten budgets.

“We have seen further growth in incentives and discounting and that’s helping affordability, but the improvement in affordability is not delivering much sales improvement,” said Jonathan Smoke, chief economist with automotive services and technology provider Cox Automotive, during a midyear review of the U.S. car market in late June. “Part of the problem is higher rates, but the other part is simply that consumers are becoming more price sensitive across many categories.”

Asp, 45, wanted to lease because he likes to drive newer cars that are still covered by warranties. But he decided to walk away because of the financing. He still has several months until his current lease runs out, so he said he is going to take his time shopping.

“There’s room to wheel and deal, but I found myself waiting,” Asp said.

The industry is in a middle space — more appealing than the last few years but not good enough to entice a large segment of people who want but don’t need a new car.

There is greater inventory of both used and new vehicles, something that had been quite a problem during the pandemic, when auto manufacturing plants were shut down and microchip shortages stalled production of new vehicles. It wasn’t too long ago that dealer showrooms were empty, stifling the inventory of trade-ins.

The available weekly amount of used cars during the first six months of the year was higher than the same time in 2023, according to Cox Automotive. In fact, the new-car supply is approaching pre-COVID levels.

Back in 2021 and 2022, it was hard for Long’s Auto Place in the east metro to keep cars in stock, with vehicles selling in a day or at most a week.

“We sold everything off and then we had to buy high and sell high,” said co-owner Justin Long, whose family has operated the dealership for more than 40 years.

Now, vehicles on the Long lot, which moved from off Rice Street in St. Paul to Hwy. 61 and County Road E East in White Bear Lake last year, might take an average of 45 days to be sold, which is a more normal cycle of turnover.

“The market has kind of leveled out compared to the craziness of two years ago, and that’s in the consumer’s favor,” Long said.

As of early July, the majority of Long’s used cars are priced under $25,000, a price point that had dwindled over the last few years.

The average transaction price of a new vehicle is about $47,300 as of May or more than a 42% increase compared with May of 2016, with discounts offered by dealers (which doesn’t include rebates) currently around $1,600 or about 25% lower, according to Edmunds. For a used vehicle for which the buyer had a loan with APR of 11.5%, the monthly payment averages $554.

“I think the sensible people are waiting or they are going to look for a used car that’s older than they expected and has more miles than they wanted,” Yoon said.

Kelley Blue Book, which is a subsidiary of Cox Automotive, forecasts new-vehicle sales for the first half of 2024 increased by nearly 225,000 units or about 3% compared to the first half of 2023.

Yet with economic uncertainty for the second half of the year, Cox Automotive forecasts new-vehicle sales will total 15.7 million, a modest gain of 1.3% from 2023.

According to Cox dealer surveys, both franchised and independent dealers had lower confidence in the strength of the selling market and the economy in the second quarter of this year than they did a year ago. They said the biggest factors holding back business were interest rates, the economy, market conditions, the political climate and expenses.

While Long acknowledges that he can’t do anything about the macro environment that could affect his business, he tries to control what he can, things like keeping his pricing competitive so that Long’s shows up high in Google searches.

Though he doesn’t know what will happen with the economy, he points out that waiting to buy a car might not produce lower prices or interest rates.

“Pick your poison,” he said. “I don’t think I’ve ever seen car prices low with interest rates low.”

link

– First Classic Car Auctions of the Year")