Africa Automotive Market Size, Share, Growth & Trends, 2033

Africa Automotive Market Size

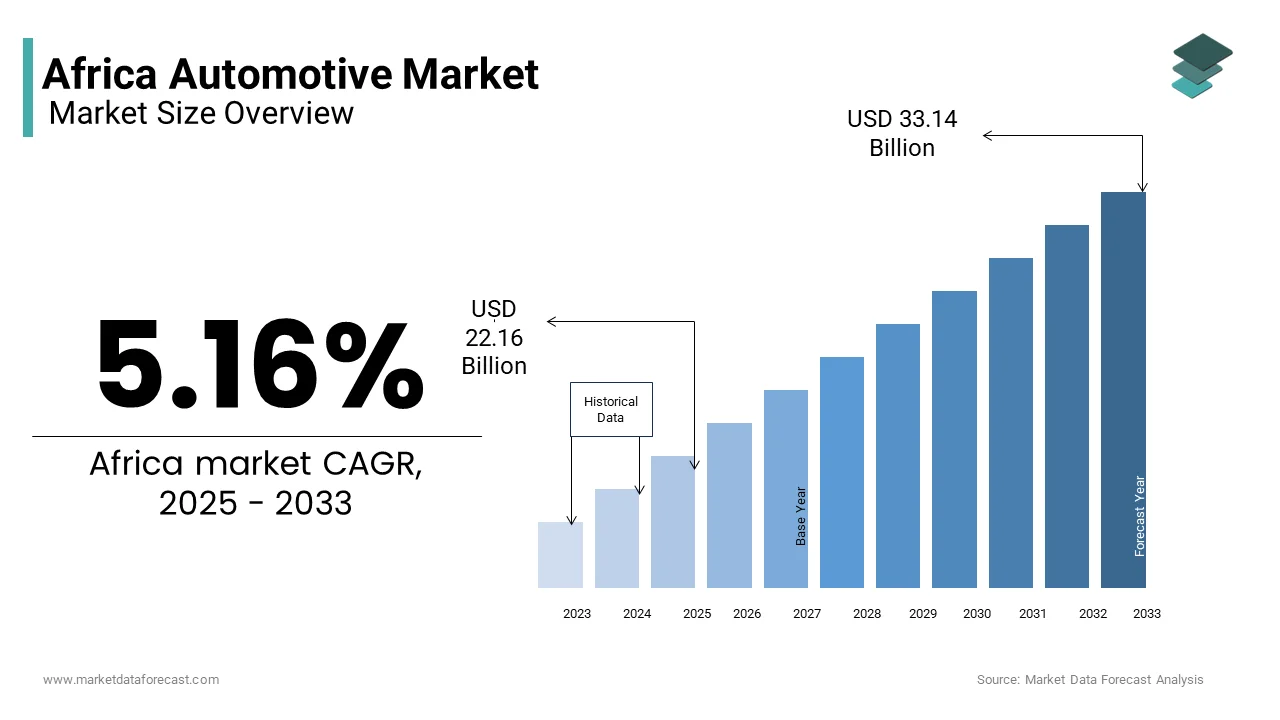

The African automotive market was valued at USD 21.07 billion in 2024 and is anticipated to reach USD 22.16 billion in 2025 to USD 33.14 billion by 2033, growing at a CAGR of 5.16% during the forecast period from 2025 to 2033.

Economic growth, urbanization, infrastructural expansion, and easier access to finance options have all had a positive effect on this quickly changing market. The high reliance on imported used cars, the lack of local manufacturing capability, and the rising interest in alternative mobility options like ride-hailing and electric vehicles are the key features of the African automotive market. According to the United Nations Economic Commission for Africa (UNECA), vehicle ownership rates remain relatively low, but rising incomes and expanding middle-class populations are steadily driving demand. The market has also seen increased participation from global automakers and regional governments aiming to boost domestic assembly operations and reduce dependency on fully built-up imports. In 2023, several countries, including Nigeria, Kenya, and Ghana, introduced policies aimed at promoting local content and improving road safety through stricter import regulations on used vehicles. Additionally, digital transformation is reshaping the automotive market, with mobile-based financing, e-commerce platforms, and digital insurance products.

MARKET DRIVERS

Rising Urbanization and Infrastructure Development

Growing infrastructural development and fast urbanization in major economies are major factors driving Africa’s automobile market. According to the United Nations, Africa’s urban population is expected to grow by nearly 50% between 2020 and 2040, and is expected to reach over 900 million people. The demand for both personal and commercial automobiles is rising as a result of this changing population. Infrastructure expansion, including road networks, logistics corridors, and urban transport systems, is further stimulating vehicle demand. People and companies are more likely to purchase cars when there are better roads and connections. Additionally, governments are prioritizing public transportation upgrades, which in turn boosts the demand for buses and minibuses. Moreover, cities such as Addis Ababa, Nairobi, and Cape Town have seen a surge in ride-hailing services like Uber and Bolt, which contributes to a growing fleet of registered vehicles.

Increasing Disposable Income and Middle-Class Expansion

The expansion of the middle class and rising disposable incomes across several African nations are playing a pivotal role in propelling the growth of the African automotive market. Customers are choosing to acquire a personal automobile more frequently as a convenience and status symbol as their purchasing power increases. According to Fitch Solutions data, the import of used cars into East Africa alone increased by 12% in 2022, with Kenya and Uganda holding the biggest shares. Moreover, banks and financial institutions are offering auto loan schemes with flexible repayment terms, which makes car ownership more accessible.

MARKET RESTRAINTS

Limited Access to Financing and Credit Facilities

Limited access to affordable financing remains a significant restraint on automotive growth in Africa. A large portion of the population still operates with informal economies, which makes it difficult to qualify for traditional bank loans or auto financing products. According to the World Bank, only 24% of adults in Sub-Saharan Africa had access to formal credit in 2022. This restricts the ability of potential buyers to purchase vehicles outright or through installment plans. Furthermore, interest rates on auto loans in many African countries remain prohibitively high. For instance, according to a 2023 report by the Central Bank of Nigeria, vehicle loan interest rates in Nigeria sometimes surpass 20%. High borrowing costs deter middle-class consumers who might otherwise be viable candidates for vehicle purchases. According to TransUnion, tighter lending requirements and growing inflation caused an 11% drop in auto credit approvals in 2022, even in comparatively established nations like South Africa. Additionally, weak credit scoring systems and a lack of financial literacy hinder lenders from extending credit confidently.

Poor Road Infrastructure and Maintenance

Inadequate road infrastructure continues to impede the automotive market’s growth. Rural and intercity roads are still in poor condition, which restricts car usage and deters investment in private transportation. In countries like Ethiopia and Malawi, poor road conditions contribute to higher vehicle maintenance costs and reduced vehicle lifespans. For example, according to 2022 research by the International Road Federation, transport companies in Zambia indicate that trucks need twice as many repairs as those working in better-maintained surroundings. Moreover, traffic congestion in major cities such as Lagos and Kinshasa leads to increased fuel consumption and wear and tear on engines. This not only raises operating costs but also deters individual buyers from investing in cars.

MARKET OPPORTUNITIES

Growth of Electric Vehicle (EV) Adoption and Green Mobility Initiatives

Increasing young population, which is expanding availability to renewable energy sources, and growing environmental consciousness are significantly promoting new opportunities for the growth of the African automotive market. Several governments across the continent are now promoting green mobility initiatives to reduce carbon emissions and dependence on imported fossil fuels. For instance, according to the Kenya Revenue Authority, Kenya implemented exemptions from taxes for EV imports in 2022 to accelerate adoption. According to BloombergNEF, EV sales in Africa are projected to reach 200,000 units annually by 2030, with early adopters concentrated in urban hubs like Cape Town, Nairobi, and Cairo. In Rwanda and Uganda, companies like Mobisol and Zembo are already using solar-powered charging stations to deploy EV delivery vans and taxis. Additionally, decentralized solar and battery storage solutions are enabling off-grid EV charging in remote areas, which opens up new markets. Africa’s plentiful sunlight and quickly growing mobile payment ecosystem make it ideally positioned to go beyond traditional fuel-based transportation and adopt sustainable mobility solutions that are suited to its particular infrastructure needs.

Expansion of Used Vehicle Import Markets and Aftermarket Services

The influx of affordable, reconditioned vehicles from Japan, Europe, and the United States is also expected to promote the growth of the African automotive market. Countries like Ghana, Kenya, and Tanzania have seen a surge in used vehicle imports, which fill the gap left by high prices for new cars. According to the United Nations Environment Programme (UNEP), over 80% of vehicles imported into Sub-Saharan Africa in 2022 were second-hand units, with Kenya alone importing more than 120,000 used cars in that year. This trend is supported by growing trade agreements and streamlined customs processes. For example, the East African Shipment Inspection Scheme (EASIS) implemented stricter emission norms for imported vehicles starting in 2023, which ensures quality while maintaining affordability. This regulatory framework enhances buyer confidence and encourages repeat purchases.

MARKET CHALLENGES

Regulatory Fragmentation Across Regional Markets

A lack of uniform laws throughout regional blocs is a quiet challenge for the growth of the African automobile market. Africa has a variety of law systems that control environmental compliance, safety regulations, taxes, and car imports. The African Continental Free Trade Area (AfCFTA) aims to streamline trade policies, but implementation remains uneven. According to the African Union, as of 2023, only 12 out of 54 member states had fully aligned their automotive import regulations with AfCFTA guidelines. For instance, while Kenya enforces strict age limits on imported used vehicles, capping them at eight years and neighboring countries like Uganda and Tanzania allow vehicles up to 15 years old. This inconsistency creates arbitrage opportunities but complicates logistics and distribution planning for automakers and distributors. Additionally, varying emission norms make it difficult for manufacturers to standardize models for pan-African deployment. Customs procedures also differ widely, with some nations imposing high tariffs on certain vehicle types. According to the Federal Inland Revenue Service (2023), tariffs on fully built-up (CBU) automobiles in Nigeria can reach over 35%, whereas South Africa offers reduced rates via SADC trade agreements.

Inconsistent Power Supply and Fuel Distribution Networks

The unstable power supply and uneven gasoline distribution infrastructure are two more significant challenges impacting the African automotive market. Many African countries still grapple with frequent electricity outages, which impact vehicle manufacturing plants, service centers, and even digital platforms facilitating vehicle sales and financing. Fuel availability and pricing volatility further exacerbate the issue. Fuel shortages are common in countries like Zimbabwe and Angola, which interfere with transportation and deter private ownership of automobiles. According to the African Energy Chamber, diesel prices in Nigeria surged by 34% in 2023 following subsidy reforms, which directly impacted commercial transport operators and fleet owners. Moreover, fuel distribution infrastructure remains underdeveloped in rural areas. This lack of accessibility hampers the performance of internal combustion engine (ICE) vehicles and constrains overall mobility. The absence of dependable electricity and fuel supply networks causes operational inefficiencies for automakers, which raises expenses and reduces customer trust in vehicle ownership.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.16% |

|

Segments Covered |

By Vehicle Type And By Region |

|

Various Analyses Covered |

Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest of Africa |

|

Market Leaders Profiled |

Toyota Motor Corporation, Volkswagen AG, Groupe Renault, Hyundai Motor Company, Ford Motor Company, Innoson Vehicle Manufacturing Company, Daimler AG, Volvo Group, Isuzu Motors Ltd, Tata Motors Limited, Ashok Leyland. |

SEGMENT ANALYSIS

By Vehicle Insights

The passenger cars segment dominated the African automotive market share in 2024. Rising urbanization and increased demand for personal mobility in key African nations are the main factors driving this segment forward. The growth of the middle class in the region is another important factor that helps market growth. According to the African Development Bank, the continent’s middle-class population reached an estimated 460 million in 2023, which increased demand for personal transportation. According to Naamsa (National Association of Automobile Manufacturers of South Africa), passenger car sales made up more than 75% of all vehicle registrations in South Africa alone in 2022, which shows a significant customer preference for private automobiles. The rise of ride-hailing services like Uber and Bolt, which have boosted the number of passenger cars entering the company market, is another contributing reason.

The commercial vehicles segment is predicted to witness a CAGR of 7.4% in the coming years, with rapidly growing logistics and e-commerce industries in the region. The growth in intra-African commerce, which is facilitated by the African Continental Free Trade Area (AfCFTA) agreement, is one of the main drivers. Additionally, urbanization and infrastructure development are boosting construction activity, which in turn increases demand for heavy-duty commercial vehicles. As per the Ethiopian Revenue and Customs Authority, the country’s commercial vehicle imports increased by 22% in 2022 as a result of government spending on road and rail developments. Moreover, last-mile delivery services are flourishing, where startups like Jumia Logistics and Sendy are expanding their fleets.

COUNTRY-LEVEL ANALYSIS

South Africa

South Africa was the top performer in the African Automotive market and accounted for 28.4% of the share in 2024. It remains the most industrialized and mature automotive market on the continent with a well-established manufacturing base and distribution network. The country’s automotive sector benefits from a well-developed financial ecosystem, which enables consumers to access vehicle financing easily. Additionally, strong domestic production supports both local consumption and exports. According to the National Association of Automobile Manufacturers of South Africa (Naamsa), Ford, BMW, and Toyota were major contributors to the 598,000 units produced locally in 2022. Prospects are also being shaped by government incentives, such as changes to import duties and EV policy frameworks.

Egypt

The Egyptian automotive market held 14.4% of the share in 2024. Egypt benefits from the advantages of a significant population and advantageous commercial connections between Africa, the Middle East, and Europe, which make it a major center in North Africa. Import substitution strategies supported by the government and intended to increase local assembly activities are one of the primary drivers. According to the Cairo Chamber of Commerce, domestic automobile sales increased by 10% in 2023 as a result of new incentives provided by the Egyptian Ministry of Industry for automakers establishing assembly factories. Additionally, economic reforms and currency devaluation have spurred demand for locally assembled vehicles. As per the Central Bank of Egypt, auto financing approvals rose by 12% in 2022, which makes car ownership more accessible to middle-income households.

Nigeria

Nigeria has a dominant African automotive market share that is expanding as a result of its sizable and youthful population, rising urbanization, and increased reliance on private transportation. One of the primary growth drivers is the high volume of used vehicles. Lagos, Abuja, and Port Harcourt have seen a surge in demand for affordable transportation solutions, particularly among the expanding middle class. Additionally, the Nigerian government launched the Automotive Industry Development Plan (AIDP) in 2023, which offers tax exemptions for local assembly plants.

Morocco

Moroccan automotive market is gaining huge traction during the forecast period. Morocco, which is positioned as a major entry point between Europe and Africa, has established a strong car manufacturing sector that draws FDI from international automakers. The Moroccan government has actively promoted the sector through industrial modernization strategies, particularly under the “Moroccan Automotive Industry Strategy 2030”. Morocco’s strategic location and affordable labor costs have allowed major firms like Renault and Stellantis to set up production plants in Tangier and Casablanca. Moreover, infrastructure development and export-oriented policies continue to enhance Morocco’s competitiveness. The government’s focus on electric mobility and green manufacturing is also paving the way for sustainable growth, which makes Morocco a pivotal player in North Africa’s evolving automotive market.

Kenya’s

The automotive market is likely to have significant growth opportunities in the coming years. Kenya is a major economic force in this region, acting as a distribution and logistics center, which boosts demand for both passenger and commercial automobiles. The development of shared mobility and ride-hailing services like Uber, Bolt, and Little Cab is a significant growth driver. According to the Kenya Revenue Authority (KRA), used vehicle imports increased by 13% in 2022, with over 120,000 units entering the country, primarily from Japan and the UAE. Additionally, urbanization and improved access to credit have boosted individual car ownership. The Standard Gauge Railway and Nairobi Expressway are two examples of infrastructure development that have increased demand for commercial transportation.

KEY MARKET PLAYERS

Toyota Motor Corporation, Volkswagen AG, Groupe Renault, Hyundai Motor Company, Ford Motor Company, Innoson Vehicle Manufacturing Company, Daimler AG, Volvo Group, Isuzu Motors Ltd, Tata Motors Limited, Ashok Leyland. Are the market players that are dominating the African automotive market?t.

Top Players In The Market

Toyota Motor Corporation

Toyota remains a dominant force in the African automotive market, which is known for its durable and reliable vehicles suited to the continent’s challenging terrain and road conditions. The company has maintained a strong presence through extensive distribution networks and localized after-sales service centers. Toyota’s reputation for producing rugged models like the Hilux and Land Cruiser has made it a preferred choice among both individual and commercial users across Africa.

Beyond vehicle sales, Toyota contributes significantly to global automotive innovation, particularly in hybrid and alternative fuel technologies. Its commitment to sustainability aligns with emerging trends in African markets seeking cleaner mobility solutions. Toyota continues to invest in regional partnerships and logistics support, which reinforce its dominant position in the continent’s evolving automotive landscape.

Volkswagen Group

Volkswagen has long been a key player in Africa, where it operates one of the largest vehicle manufacturing plants outside of Europe. The brand’s success stems from its ability to localize production and tailor models to regional preferences. Volkswagen Group South Africa, a subsidiary, is a key contributor to employment generation and export-driven expansion.

Globally, Volkswagen is at the forefront of electric vehicle development and digital transformation in mobility. Its strategic focus on electrification is gradually influencing its product offerings in African markets. Volkswagen expands its presence in the area and advances global automotive technology at the same time by making ongoing investments in dealer infrastructure and customer interaction.

Renault-Nissan-Mitsubishi Alliance

The Renault-Nissan-Mitsubishi Alliance holds a significant position in the African automotive market, particularly in North and West Africa. Renault has established itself as a leader in affordable and fuel-efficient vehicles, which caters to a broad consumer base. Shared technological platforms allow for faster market access and more affordable production for the alliance.

In the global market, the alliance is driving innovation in electric mobility and autonomous driving technologies. These developments are gradually being introduced into African markets, especially in urban areas where demand for sustainable transport is rising. The alliance’s collaborative approach allows it to maintain a competitive edge by leveraging synergies across brands, which enhances supply chain efficiency and expands regional dealership networks.

Top Strategies Used By Key Market Participants

One of the most prevalent strategies among leading automakers in Africa is local assembly and manufacturing partnerships, which allow companies to reduce import costs, comply with regulatory frameworks, and cater to local consumer preferences. Companies may sell competitively priced cars and take advantage of government subsidies by establishing or growing assembly factories in nations like South Africa, Egypt, and Nigeria.

Another key strategy is expanding financing and leasing options to make vehicle ownership more accessible. Affordability issues that have traditionally restricted market expansion are addressed by major companies working with banks and financial institutions to offer flexible payment options.

Lastly, Automakers are incorporating online portals and mobile applications into their digital sales and after-sales support platforms to improve the customer experience. This change helps companies increase their market presence and client loyalty by facilitating effective inventory management, real-time service scheduling, and remote diagnostics.

COMPETITION OVERVIEW

Competition in the African automotive market is intensifying as global and regional players vie for market share in an environment marked by diverse consumer needs, evolving regulatory landscapes, and infrastructural challenges. Established international brands such as Toyota, Volkswagen, and Renault continue to dominate due to their strong brand recognition, robust distribution networks, and localized manufacturing capabilities. These firms leverage economies of scale and well-established after-sales service systems to maintain a competitive edge.

Simultaneously, emerging domestic and regional manufacturers are gaining traction by offering cost-effective alternatives tailored to local conditions. The rise of used vehicle imports also presents a unique competitive dynamic, which allows consumers access to affordable transportation without the high cost of new cars. In response, major automakers are adapting by introducing budget-friendly models and investing in localized marketing strategies.

Additionally, competition extends beyond traditional sales, with companies focusing on after-sales services, digital customer engagement, and sustainable mobility solutions. Automakers are rushing to release electric and hybrid vehicles that are appropriate for African climates as governments push for cleaner transportation rules. This evolving competitive market shows the need for agility, innovation, and deep market understanding to sustain long-term growth.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Toyota launched a localized version of its Hilux pickup truck in Kenya, which was designed specifically to meet the durability and performance demands of African roads by enhancing its appeal among commercial users and private buyers alike.

- In June 2023, Volkswagen announced a strategic partnership with a South African energy firm to develop EV charging infrastructure, which supports the gradual rollout of electric mobility solutions in key urban centers.

- In November 2023, Renault expanded its dealership network in Nigeria by opening over 15 new service centers across major cities to improve customer accessibility and reinforce brand presence in West Africa.

- In March 2024, Nissan entered into a joint venture with a local logistics company in Ghana to deploy a fleet of electric delivery vans, which aims to promote sustainable commercial transport solutions in the region.

- In September 2024, the Mitsubishi group introduced a mobile-based vehicle financing platform in Egypt that allows prospective buyers to apply for loans remotely, thereby increasing accessibility and boosting sales conversion rates.

MARKET SEGMENTATION

This research report on the African automotive market is segmented and sub-segmented into the following categories.

By vehicle Type

- Passenger Cars

- Commercial Vehicles

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest of Africa

link

– First Classic Car Auctions of the Year")