Europe ADAS Market Size

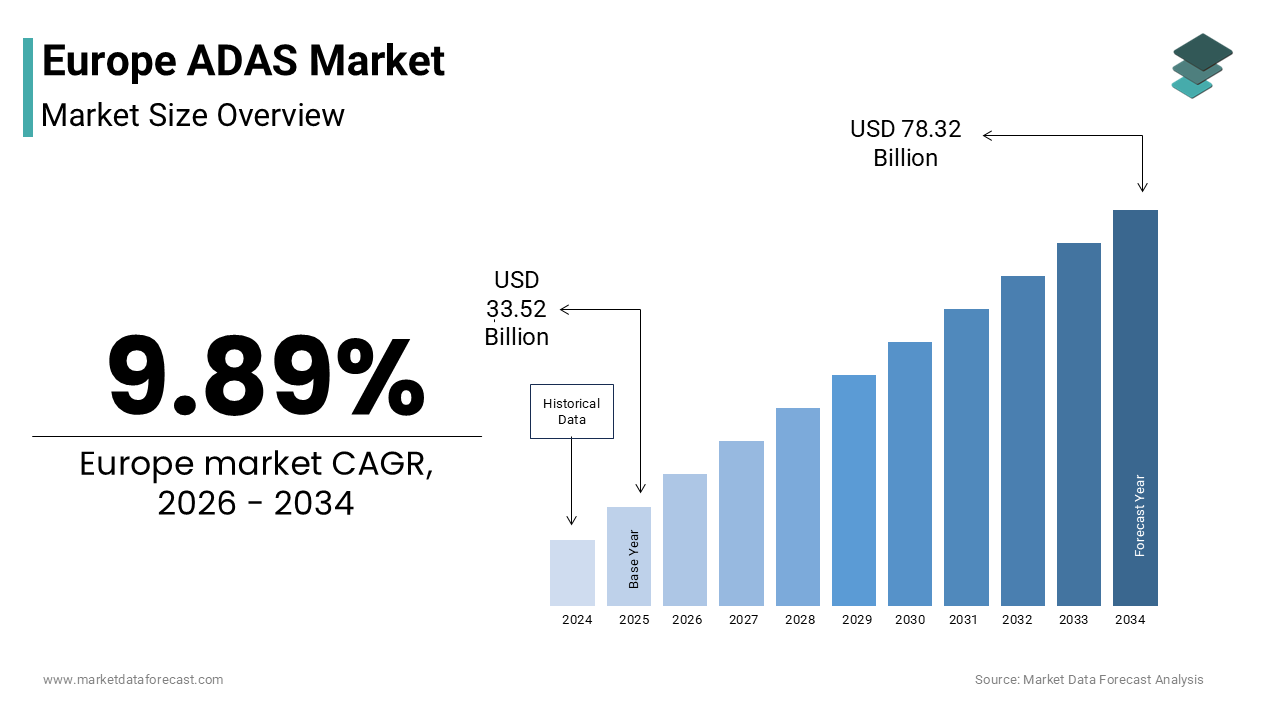

The Europe ADAS market size was valued at USD 33.52 billion in 2025 and is anticipated to reach USD 36.83 billion in 2026 from USD 78.32 billion by 2034, growing at a CAGR of 9.89% during the forecast period from 2026 to 2034.

Advanced Driver Assistance Systems (ADAS) are a collection of electronic technologies integrated into vehicles to enhance safety by reducing human error and improving driving comfort. These systems include automatic emergency braking, lane keeping assist, adaptive cruise control, blind spot detection, and traffic sign recognition, among others. The European ADAS market is uniquely shaped by stringent regulatory mandates from the European Commission and the United Nations Economic Commission for Europe (UNECE). The European Transport Safety Council emphasizes that thousands of people still lose their lives annually in road crashes across the EU, highlighting a slow decline in progress that fails to meet EU, long-term, policy-driven safety goals. Under EU General Safety Regulation 2019/2144, new vehicle types introduced to the market in the EU are required to feature advanced driver assistance systems, including intelligent speed assistance and lane-keeping assistance, as standard equipment, with this mandate extending to all new vehicles sold in later years. Furthermore, Euro NCAP’s five star safety rating now requires robust ADAS performance for top scores, directly influencing consumer purchasing behaviour. This confluence of binding legislation, safety advocacy, and consumer awareness has made Europe the most regulated and technologically advanced ADAS market globally, where compliance is not optional but foundational to vehicle homologation.

MARKET DRIVERS

Mandatory Regulatory Requirements Accelerating ADAS Adoption

The comprehensive and enforceable regulatory framework imposed by the European Union and UNECE, which mandates specific ADAS features on all new vehicles, is a major driver of the European ADAS market. Following the introduction of updated EU safety regulations in the early 2020s, newly approved and subsequently all new vehicles are required to feature enhanced, standardized safety systems—such as automated emergency braking and driver monitoring tools—to minimize human error. According to the European Commission, these measures are projected to prevent over 25,000 road deaths and 140,000 serious injuries by 2038. The regulation applies uniformly across all 27 member states, creating a de facto baseline for every vehicle sold. Automakers cannot opt out. Compliance is a prerequisite for market access. This legal compulsion has transformed ADAS from a premium differentiator into a universal necessity, ensuring near 100% penetration of core systems in new vehicles. Consequently, suppliers such as Bosch, Continental, and Valeo have scaled production capacity across Germany, France, and Romania to meet guaranteed demand, turning regulatory enforcement into the single largest engine of market growth.

Consumer Demand for Enhanced Safety and Convenience Features

Rising consumer expectations for safety and driving comfort are significantly amplifying ADAS adoption, beyond regulation, which acts as an accelerator of the Europe ADAS market. This trend is particularly evident in mid and high-end vehicle segments. European consumers are increasingly treating advanced driver assistance systems as essential features, rather than optional luxuries, with safety technology becoming a primary influencer in new vehicle purchasing decisions. European vehicle buyers are showing a rising willingness to invest in premium, convenience-focused driving features, including automated parking and adaptive cruise control, to enhance comfort and safety. This sentiment is reinforced by insurance incentives. Insurers in the UK and Germany are encouraging the adoption of certified advanced driver assistance systems by providing lower insurance premiums for vehicles that demonstrate enhanced safety capabilities. Moreover, urban congestion and aging populations in Western Europe heighten demand for stop and go cruise control and rear cross traffic alert. Automakers respond by bundling ADAS into trim levels rather than standalone options, normalizing their presence even in entry level models. This market pull, synergistic with regulatory push, ensures sustained innovation and integration depth beyond minimum legal requirements.

MARKET RESTRAINTS

High System Costs and Integration Complexity Constraining Mass Market Penetration

The elevated cost and engineering complexity associated with higher level systems, particularly those requiring sensor fusion and high-performance computing, is a significant restraint on the Europe ADAS market. While basic ADAS like lane departure warning are now commoditized, advanced functions such as highway assist or urban automated driving demand multiple radar cameras ultrasonic sensors and domain controllers, adding 800 to 2,500 euros to vehicle bills of materials. According to the German Automotive Industry Association, this cost burden disproportionately affects small and low margin vehicles, delaying full ADAS rollout in budget segments. Furthermore, integrating these systems into legacy vehicle architectures requires extensive validation and recalibration, extending development cycles by six to twelve months. Smaller European automakers like Dacia or Skoda face particular challenges in amortizing these costs across lower volume platforms. High integration costs mean the full range of ADAS features will stay tied to premium vehicle prices, preventing widespread safety benefits across the entire, diverse, vehicle market.

Fragmented Sensor and Software Standards Hindering Interoperability

The lack of harmonized technical standards for ADAS sensors, data formats, and over-the-air update protocols is a critical barrier to system reliability, future-proofing, and the European ADAS market. While regulations mandate outcomes, such as collision avoidance, they do not prescribe sensor types or software architectures, leading to proprietary implementations by each OEM. According to the European New Car Assessment Programme, this fragmentation results in inconsistent performance; for example, automatic emergency braking systems exhibit varying activation thresholds and false positive rates across brands. Moreover, the absence of standardized cybersecurity protocols for ADAS software updates creates vulnerabilities, as highlighted by the EU Agency for Cybersecurity’s 2023 threat assessment. This heterogeneity complicates third party servicing, increases recall risks, and impedes the development of universal validation tools. Failure to align on core technical interfaces threatens to cause inefficiency, consumer confusion, and delays in deploying next-gen cooperative ADAS that rely on vehicle-to-infrastructure communication.

MARKET OPPORTUNITIES

Expansion of Urban Automated Driving Functions for City Environments

The development and deployment of Level 2+ and Level 3 automated driving systems tailored for complex European urban environments pave the way for new opportunities for the Europe ADAS market. Unlike highway automation, city driving demands precise localization, pedestrian intent prediction, and interaction with cyclists and trams, scenarios where European cities offer rich real world testing grounds. European smart city initiatives are actively fostering extensive, collaborative pilot projects across major cities to test and validate automated valet parking and low-speed urban mobility solutions. The European Union’s Horizon Europe framework is investing heavily in urban mobility automation through 2027, with substantial funding dedicated to advancing AI-based perception and Vehicle-to-Everything (V2X) communication technology to enhance urban infrastructure. Companies like Mobileye and ZF are already deploying REM crowdsourced mapping in European cities to build high definition localization layers. The drive for sustainable, low-congestion urban mobility is accelerating the use of automated shuttles and delivery bots, creating new ADAS revenue opportunities and turning city streets into living laboratories for advanced vehicle technology.

Integration of ADAS with Electrification and Vehicle to Grid Ecosystems

The convergence of ADAS with electric vehicle platforms and smart grid infrastructure provides a strong opening for the Europe ADAS market. Electric vehicles, with their centralized electronic architectures and high voltage systems, provide an ideal foundation for advanced ADAS due to simplified wiring and abundant power for sensors and computers. Driven by advanced technology integration, new electric vehicles sold in the European Union are increasingly equipped with higher-level driver assistance features compared to traditional combustion models, reflecting a faster adoption rate of automated systems in the electric segment. More significantly, ADAS data on driving patterns, location, and energy use can be leveraged for vehicle to grid services. For instance, predictive routing from navigation ADAS can optimize charging schedules based on grid load and renewable availability. Pilot programs in the Netherlands and Denmark are already using ADAS derived trip data to manage EV charging in residential areas. This synergy positions ADAS not just as a safety layer but as an intelligent node in the broader energy and mobility ecosystem, unlocking value through data monetization and grid stability services.

MARKET RESTRAINTS

Cybersecurity Vulnerabilities in Connected ADAS Architectures

The escalating risk of cyberattacks targeting connected driver assistance systems degrades the growth of the Europe ADAS market. As ADAS evolves toward over the air updatable, cloud connected platforms, it expands the attack surface for malicious actors. The automotive industry is experiencing a significant increase in high-impact cyber incidents, driven by malicious actors using remote techniques to manipulate vehicle sensors, which threatens to compromise safety-critical functions like automated braking and steering. Unlike mechanical failures, cyber compromises can be remotely triggered at scale, posing systemic safety risks. Current EU type approval processes lack mandatory penetration testing for ADAS software stacks, leaving gaps in certification. Moreover, the long vehicle lifecycle means many ADAS units will operate on outdated firmware, vulnerable to newly discovered exploits. The absence of enforceable UNECE R155 cybersecurity standards threatens to erode consumer trust, which could trigger regulatory backlash, create liability crises, and stifle innovation across the ADAS sector.

Data Privacy and Ethical Dilemmas in AI Driven Decision Making

The proliferation of camera based ADAS raises profound challenges around data privacy and algorithmic ethics under the region’s strict General Data Protection Regulation, which inhibits the expansion of the Europe ADAS market. Systems that continuously record and process images of pedestrians license plates and public spaces generate vast amounts of personal data, triggering GDPR compliance obligations. European data protection authorities are increasing pressure on automobile manufacturers to improve privacy safeguards by requiring better anonymization of both interior and exterior vehicle camera footage to protect the privacy of passengers and bystanders. Beyond privacy, ethical questions persist about how ADAS algorithms prioritize actions in unavoidable crash scenarios, a dilemma known as the “trolley problem.” The EU’s proposed Artificial Intelligence Act classifies ADAS as high risk AI, requiring transparency in decision logic and human oversight. However, proprietary black box models make such disclosure commercially sensitive. Navigating this tension between safety efficacy and fundamental rights could delay deployments, increase compliance costs, and fragment development approaches across member states, ultimately slowing the pace of life saving automation in one of the world’s most privacy conscious regions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

9.89% |

|

Segments Covered |

By System Type, Sales Channel, Vehicle Type, Drugs and Region |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Bosch, Continental, Denso, Valeo, ZF Friedrichshafen, Autoliv, Aptiv, Magna International, Mobileye (an Intel company), Delphi Technologies (BorgWarner), Infineon Technologies, NXP Semiconductors, and Hella (Forvia Group). |

SEGMENTAL ANALYSIS

By System Type Insights

The adaptive cruise control (ACC) segment combined with lane keeping assist segment held the majority share of 38.6% of the European ADAS market in 2025. This dominance is driven by its dual role as both a regulatory requirement and a highly valued driver comfort feature on highways and interurban roads. Under the EU General Safety Regulation, all new vehicles must include intelligent speed assistance and lane departure warning—functions that form the foundation of these systems. Euro NCAP reports that lane support technologies are now standard on most new passenger cars, resulting in high safety ratings across the European market. Furthermore, the extensive, high-quality motorway infrastructure spanning Europe offers suitable conditions for the application of advanced cruise control technologies. The German motorway network, featuring sections without mandatory maximum speeds, necessitates diligent speed management and creates a high-utilization environment for adaptive cruise control systems. German and French automakers have integrated these systems into base trims across mid size sedans and SUVs, making them standard rather than optional. The seamless fusion of radar and camera data enables smooth longitudinal and lateral control, reducing driver fatigue on long journeys, a key selling point in Europe’s aging driving population.

The automated emergency braking (AEB) systems segment is predicted to witness the highest CAGR of 18.4% from 2026 to 2034 due to the EU’s binding mandate requiring AEB with vulnerable road user detection on all new vehicles. In the EU, road deaths are highest among car occupants; however, pedestrians account for a critical proportion of fatalities, a trend concentrated in urban settings. Euro NCAP now awards zero stars to any vehicle without robust AEB performance in urban scenarios up to several kilometers per hour. Suppliers like Mobileye and Bosch have responded by deploying high resolution cameras and AI based object classification that distinguish between adults children cyclists and even animals. Real-world data from Sweden indicates that the widespread implementation of advanced emergency braking systems designed to detect pedestrians is effectively reducing the risk of collisions, with particularly high effectiveness in specific urban settings such as intersections and during adverse weather conditions. This life saving efficacy, backed by regulation and consumer trust, ensures exponential adoption beyond compliance minimums.

By Sales Channel Insights

The OEM fitted ADAS systems segment dominated the Europe ADAS market by accounting for a substantial share in 2025. The dominance of the OEM fitted ADAS systems segment is attributed to the deep integration of ADAS into vehicle electronic architectures during manufacturing, which ensures sensor calibration, software validation, and functional safety compliance that aftermarket solutions cannot replicate. Crucially, EU type approval regulations require ADAS functions to be certified as part of the original vehicle design; retrofitting core systems like AEB or lane keeping after sale does not satisfy homologation requirements. According to the European Commission, no new vehicle can receive type approval without factory installed ADAS meeting UNECE Regulation No 157 standards. Major automakers like Volkswagen Stellantis and BMW embed ADAS domains directly into their vehicle operating systems, enabling over the air updates and sensor fusion across radar cameras and ultrasonics. Insurance providers such as Allianz also only recognize OEM systems for safety discounts, further disincentivizing aftermarket alternatives. This regulatory and technical lock in makes OEM channels the sole viable route for advanced ADAS deployment.

The aftermarket retrofit segment is estimated to register the fastest CAGR of 12.1% during the forecast period owing to commercial fleets and older passenger vehicles where factory ADAS was unavailable but operational safety and insurance incentives drive upgrades. Logistics companies like DHL and PostNL are retrofitting blind spot detection and rear cross traffic alert on delivery vans to protect cyclists in dense urban centers. Due to the high vulnerability of cyclists in urban traffic, particularly in collisions with large vehicles, major European cycling cities have introduced strict requirements for trucks to install enhanced safety technology. This trend, supported by advocacy groups, mandates the retrofitting of camera monitor systems and blind-spot sensors to improve driver visibility and reduce fatalities at intersections. Additionally, insurers such as AXA offer premium reductions for fleet operators who install certified aftermarket AEB. Regulatory shifts also help; the EU’s upcoming revision of the Periodic Technical Inspection directive may soon require ADAS functionality checks, creating a service opportunity for garages. he growing, aging population of cars across Europe presents a major safety challenge that, while addressed through limited, foundational technology, remains a critical gap in vehicular safety.

By Vehicle Type Insights

In 2025, the passenger cars segment was the largest segment in the Europe ADAS market and occupied a significant share. The leading position of the passenger cars segment is supported by both regulatory focus and market dynamics; EU safety mandates apply first and foremost to M1 category vehicles, and consumer demand for safety features is strongest in private car ownership. Driven by safety regulations, new passenger cars registered in the European Union are increasingly standard-equipped with a wider array of driving assistance technologies, highlighting a significant, rapid, and widespread adoption of active safety features across the market. Premium brands like Mercedes Benz and Volvo have made Level 2 automation standard across entire lineups, while volume manufacturers such as Renault and Skoda bundle basic ADAS into entry level trims to meet Euro NCAP five star requirements. The average number of safety assistance systems featured in new European cars has risen dramatically over the past few years, indicating a swift shift from optional to mandatory, standard-fitment driver-assist technologies. This mass integration, driven by legislation and competitive positioning, establishes passenger cars as the foundational platform for ADAS proliferation across the continent.

The light commercial vehicles segment is anticipated to witness the fastest CAGR of 21.3% from 2026 to 2034. The swift expansion of the light commercial vehicles segment is propelled by the EU’s extension of General Safety Regulation requirements to N1 category vehicles starting in 2024, mandating AEB lane departure warning and drowsiness detection on all new vans. Light commercial vehicles are increasingly involved in fatal urban crashes, according to safety research regarding urban road traffic. Fleet operators like Amazon and UPS are accelerating adoption to reduce liability and insurance costs. Equipping European delivery van fleets with automated emergency braking has shown a notable decrease in urban collisions. Moreover, municipal low emission zones in cities like Paris and Berlin increasingly require safety certifications for commercial access. This confluence of regulation operational necessity and urban policy is transforming the LCV segment from an ADAS laggard into the highest growth vector in the European market.

REGIONAL ANALYSIS

Germany ADAS Market Analysis

Germany led the Europe ADAS market and captured a 24.9% share in 2025. The demand for ADAS in Germany is credited to its position as home to premium automakers like BMW, Mercedes-Benz, and Volkswagen, which pioneered advanced driver assistance and continue to integrate cutting-edge sensor suites as standard. Germany’s high rate of motorized vehicle ownership and dense car population create favorable conditions for the widespread adoption of advanced driver assistance systems. According to German road safety research, the adoption of Advanced Driver Assistance Systems, specifically those with automatic emergency braking capabilities, is contributing to a decrease in rear-end collisions on federal highways. Furthermore, Germany actively shapes EU regulations through its representation in UNECE working groups, ensuring technical feasibility aligns with industrial capability. The country also hosts major ADAS suppliers including Bosch and Continental, whose R&D centers in Stuttgart and Frankfurt drive innovation in sensor fusion and AI perception. This ecosystem of regulation manufacturing and technology cements Germany’s role as the undisputed engine of Europe’s ADAS evolution.

France ADAS Market Analysis

France was the second largest country in the Europe ADAS market and occupied a share of 19.5% in 2025. The growth of the French market is fuelled by its success in democratizing ADAS across affordable vehicle segments. Automakers like Stellantis and Renault have embedded core ADAS functions, including automatic emergency braking and lane keep assist, into entry level models such as the Peugeot 208 and Dacia Sandero, achieving near 100% penetration in new sales. According to France’s Road Safety Observatory (ONISR), the continued deployment of modernized speed enforcement systems, combined with a return to pre-pandemic traffic behavior, has helped stabilize and slightly reduce fatal accidents on rural roads in the early 2020s, following the initial sharp drop during the pandemic-related travel restrictions. France also enforces strict insurance incentives. The Fédération Française des Sociétés d’Assurances mandates ADAS verification for premium discounts, accelerating consumer adoption. Additionally, Paris’s aggressive urban mobility policies, including restrictions on non ADAS equipped delivery vans in the city center, drive commercial uptake. This blend of industrial strategy public policy and behavioral economics makes France a model for equitable ADAS diffusion beyond luxury segments.

United Kingdom ADAS Market Analysis

The United Kingdom holds a significant position in the Europe ADAS market due to its strong road safety advocacy and influential insurance sector. Although no longer an EU member, the UK has retained and even expanded EU ADAS mandates, requiring AEB and lane departure warning on all new vehicles since 2022. Thatcham Research, the UK’s automotive safety authority, plays a pivotal role by independently testing ADAS performance and publishing results that directly impact insurance group ratings. Major insurance bodies in the UK recognize that vehicles equipped with validated Autonomous Emergency Braking systems, such as those tested by Thatcham, qualify for lower insurance risk groupings, offering substantial premium incentives for consumers. The UK also leads in fleet adoption. Large-scale commercial fleets operated by organizations like Royal Mail and BT have implemented extensive retrofitting of advanced safety systems, including blind spot detection, to enhance the protection of vulnerable road users in urban environments. This unique synergy between independent safety assessment insurer influence and fleet operator pragmatism ensures the UK remains a high integrity and rapidly evolving ADAS market.

Italy ADAS Market Analysis

Italy expanded steadily in the European market, with ADAS adoption uniquely driven by complex urban environments and commercial fleet modernization. Italian cities like Rome and Milan feature narrow streets high scooter density and frequent pedestrian interactions, creating demand for low speed AEB and parking assist systems. According to ISTAT and ACI reports, urban accidents involving e-scooters in Italy continued to rise, with both total accidents and fatalities increasing between 2022 and 2023. Fiat Professional and Iveco have responded by equipping their Ducato and Daily vans with 360 degree camera systems and rear cross traffic alert as standard. Italy also leads in aftermarket innovation. Companies like Magneti Marelli offer certified retrofit kits for historic vehicles exempt from new regulations but used daily in city centers. This focus on real world urban safety challenges positions Italy as a laboratory for context specific ADAS solutions tailored to Southern Europe’s distinctive mobility patterns.

Sweden ADAS Market Analysis

Sweden is predicted to grow in the Europe ADAS market from 2026 to 2034. It is renowned globally for its Vision Zero policy that treats all traffic fatalities as system failures. This philosophy has made Sweden an early and enthusiastic adopter of life saving ADAS technologies. Volvo Cars, headquartered in Gothenburg, was the first automaker to make automatic emergency braking standard across its entire lineup in 2014, setting a benchmark later adopted EU wide. The widespread adoption of autonomous emergency braking systems, capable of detecting pedestrians, has contributed to a substantial decrease in pedestrian crash risks in Sweden, particularly in daylight and urban environments. Sweden also hosts extensive winter testing facilities where ADAS performance is validated under extreme conditions, critical for radar and camera reliability in snow and ice. The country’s collaboration between government industry and academia through initiatives like Drive Sweden accelerates real world trials of connected ADAS. This culture of safety by design and empirical validation makes Sweden a trusted proving ground for next generation driver assistance systems in Europe.

COMPETITIVE LANDSCAPE

The Europe ADAS market features intense competition among established Tier 1 suppliers, specialized technology firms, and increasingly, in house OEM software divisions. Bosch Continental and ZF dominate the hardware integration space, leveraging decades of automotive relationships and manufacturing scale. Meanwhile, companies like Mobileye and NVIDIA compete on AI algorithms and computing platforms, offering differentiated software stacks. European automakers such as Mercedes Benz and BMW are also developing proprietary ADAS software to retain control over user experience and data. The market is characterized by rapid technological iteration, stringent safety certification requirements, and high barriers to entry due to functional safety and cybersecurity mandates. Collaboration often coexists with competition as firms form consortia to share validation costs and infrastructure. Ultimately, success hinges on balancing regulatory compliance, system reliability, and scalable economics in a landscape where safety performance is non negotiable and public scrutiny is high.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe ADAS market include

- Bosch

- Continental

- Denso

- Valeo

- ZF Friedrichshafen

- Autoliv

- Aptiv

- Magna International

- Mobileye (an Intel company)

- Delphi Technologies (BorgWarner)

- Infineon Technologies

- NXP Semiconductors

- Hella (Forvia Group)

Top Players in the Market

Robert Bosch GmbH

Robert Bosch GmbH is a German multinational engineering and technology company that stands as a leading developer and supplier of Advanced Driver Assistance Systems in Europe. The company provides a comprehensive portfolio including radar cameras ultrasonic sensors and central control units that power adaptive cruise control automated emergency braking and parking assist across major European automakers. Bosch has strengthened its position by investing heavily in artificial intelligence and software defined vehicle architectures enabling over the air updates and sensor fusion capabilities. The company also collaborates closely with EU regulatory bodies to shape technical standards for ADAS validation. These initiatives reinforce Bosch’s role as a foundational technology enabler not only in Europe but globally where its ADAS platforms are deployed in vehicles across North America and Asia.

Continental AG

Continental AG is a German automotive parts manufacturer renowned for its advanced driver assistance and automated driving solutions tailored to European road conditions and regulatory frameworks. The company supplies scalable ADAS systems ranging from basic camera modules to high performance domain controllers for Level 2+ automation. Continental has reinforced its market presence by expanding its AI driven data processing capabilities through its subsidiary Elektrobit and by establishing dedicated cybersecurity protocols compliant with UNECE Regulation No 155. It also partners with European cities on pilot projects for connected ADAS in urban environments. These strategic moves position Continental as a key integrator of safe secure and future ready driver assistance technologies across global OEM platforms.

Mobileye, an Intel Company

Mobileye, an Intel company headquartered in Israel with major R&D centers in Germany and France, is a pioneer in vision based ADAS using proprietary EyeQ chipsets and Road Experience Management mapping technology. In Europe, Mobileye’s systems are embedded in millions of vehicles from premium and volume manufacturers alike, providing functions such as lane keeping traffic sign recognition and collision avoidance. The company has strengthened its European footprint by launching its Responsibility Sensitive Safety model to address ethical decision making in automated driving and by collaborating with Euro NCAP on next generation assessment protocols. Mobileye’s focus on camera centric affordable scalability ensures its continued influence in shaping accessible and certifiable ADAS standards worldwide.

Top Strategies Used by the Key Market Participants

Key players in the Europe ADAS market are primarily focused on developing scalable software defined architectures that support over the air updates and sensor fusion across radar camera and lidar modalities. Companies are investing heavily in artificial intelligence for object detection and path prediction while ensuring compliance with UNECE Regulation No 155 on cybersecurity and No 157 on automated lane keeping. Strategic partnerships with automakers cities and regulatory bodies are critical to co develop validation protocols and real world testing frameworks. Additionally firms are expanding data collection through crowdsourced mapping and simulation to train robust perception models. Emphasis on functional safety ISO 26262 certification and ethical AI governance further differentiates leading suppliers in this highly regulated and safety critical environment.

MARKET SEGMENTATION

This research report on the Europe ADAS market has been segmented and sub-segmented based on the following categories.

By System Type

- Parking Assist Systems

- More

By Sales Channel

- OEM Fitted

- Aftermarket Retrofit

By Vehicle Type

- Two Wheelers

- Passenger Cars

- More

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link